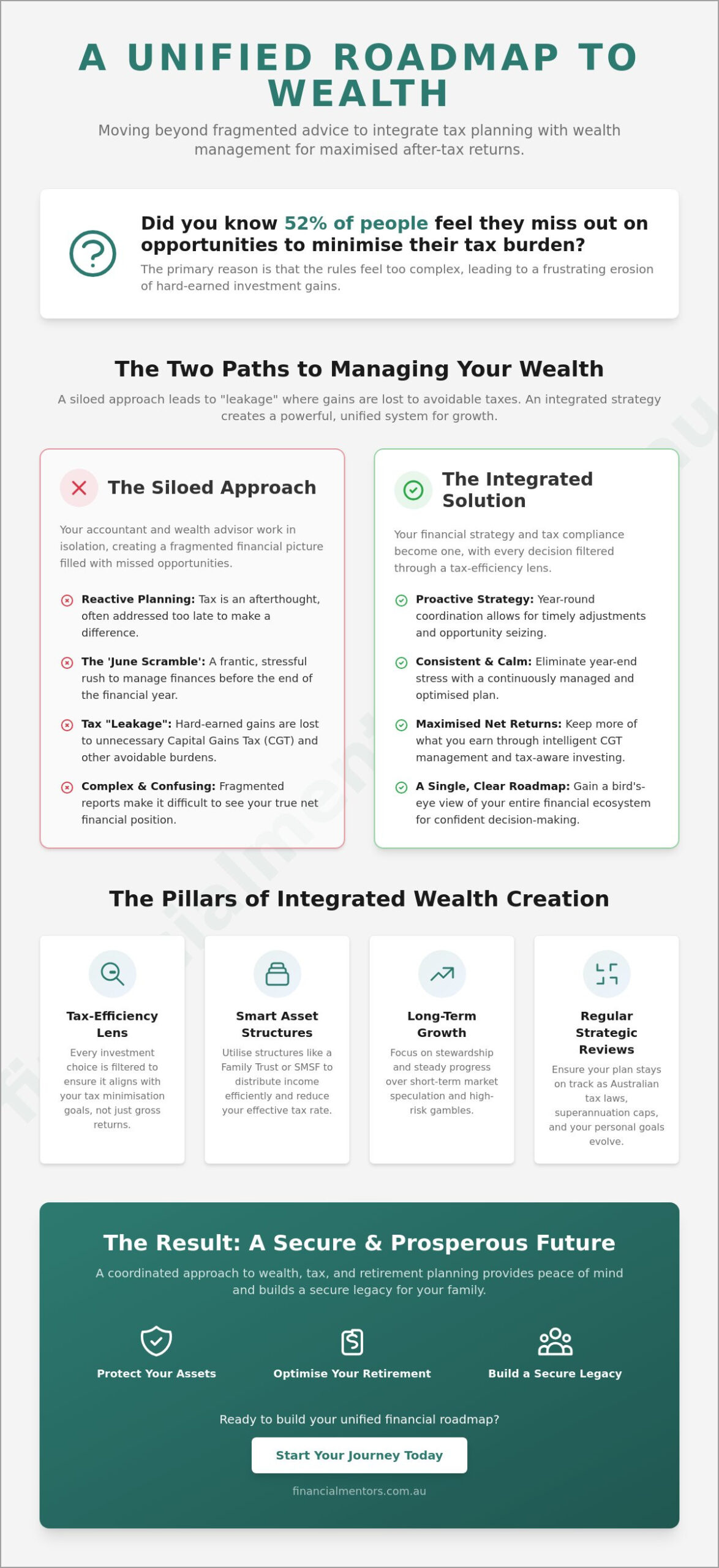

Did you know that 52% of people feel they are missing out on opportunities to minimise their tax burden simply because the rules feel too complex? It is a common frustration to watch your hard-earned investment gains be eroded by tax, especially when you are already managing the intricacies of Superannuation and Division 293. If you have ever felt that your financial life lacks a unified roadmap, you aren’t alone. The key to moving forward with confidence lies in integrating tax planning with wealth management to ensure every part of your portfolio works in harmony.

We understand that you want more than just a growing balance; you want the peace of mind that comes from knowing your family’s future is secure. By shifting from a reactive approach to a proactive strategy, you can simplify your decision-making and focus on what truly matters. In this guide, we will show you how a coordinated approach can protect your assets, optimise your retirement, and provide a clear path toward a lasting legacy. Let’s explore how a strategic partnership can help you achieve the maximised after-tax returns you have worked so hard for in 2026.

Key Takeaways

- Understand why moving away from siloed advice between your accountant and advisor prevents missed opportunities and simplifies your financial roadmap.

- Discover how integrating tax planning with wealth management creates a unified system that filters every investment decision through a tax-efficiency lens.

- Learn how year-round coordination can replace the stressful ‘June scramble’ and significantly improve your net returns through proactive Capital Gains Tax management.

- Explore the ‘Mentorship Factor’ and why having a trusted guide who understands your unique life goals offers more value than a generic robo-advisor.

- Gain clarity on how a coordinated approach to wealth, tax, and retirement planning helps protect your assets and build a secure legacy for your family.

What Does Integrating Tax Planning with Wealth Management Really Mean?

Have you ever felt like your financial life is a collection of separate puzzle pieces that don’t quite fit together? For many Australians, wealth creation happens in one office while tax preparation happens in another. This fragmented approach often leads to “leakage” where hard-earned gains are lost to avoidable taxes. When we explore the foundational question of What is Wealth Management?, it becomes clear that true success requires a blend of investment strategy and tax precision.

Truly integrating tax planning with wealth management means your financial strategy and your tax compliance are no longer strangers. It is a unified system where your long-term goals are protected by a deep understanding of the Australian tax landscape. To ensure you are receiving advice you can trust, look for the Australian Financial Services Licence (AFSL). This licence is the benchmark for professional advice in Australia; it ensures your advisor meets strict legal and ethical standards designed to protect your interests.

The Hidden Costs of Disjointed Financial Advice

Siloed advice is a common trap. Your accountant might see your tax return in July, but by then, the opportunity to offset a capital gain from March has already passed. This reactive planning leads to unnecessary Capital Gains Tax (CGT) and a feeling of constant catch-up. The benefit of integrating tax planning with wealth management is that it replaces fragmented reports with a single, clear financial roadmap. Instead of worrying about the complexity of Division 293 or Superannuation caps in isolation, you gain a bird’s-eye view of your net position, allowing for proactive adjustments throughout the year rather than a frantic scramble in June.

Stewardship: The Heart of Professional Wealth Management

Professional wealth management goes beyond mere stock picking. It involves managing your total financial ecosystem, from family trusts to retirement income streams. This is where the concept of stewardship becomes vital. It’s about acting as a wise guide for your assets to ensure they serve you now and your loved ones later. By upholding high professional standards, you aren’t just chasing returns; you are future-proofing your family’s stability and ensuring your legacy is handled with care.

Stewardship is the responsible management of wealth across generations.

The Pillars of Integrated Wealth Creation Strategies

If you’ve ever wondered why some portfolios seem to grow faster than others, the answer often lies in the hidden mechanics of tax. Building wealth isn’t just about the gross return on an investment; it’s about what you actually keep after the Australian Taxation Office (ATO) has taken its share. By integrating tax planning with wealth management, every investment choice you make is filtered through a tax-efficiency lens. This ensures that you aren’t just collecting assets, but building a robust financial ecosystem that works for your specific life stage.

A well-constructed Australian portfolio requires more than just a mix of shares and property. It demands a sophisticated approach to diversification that accounts for our unique tax environment. For instance, the way you handle franking credits or capital gains discounts can have a profound impact on your long-term results. Rather than chasing short-term market speculation, a wise mentor focuses on a “Long-Term Growth” mindset. This approach values steady progress and stewardship over high-risk gambles. Because Australian laws and contribution caps evolve frequently, regular strategic reviews are essential to keep your plan on track. If you are wondering how your current portfolio would perform under a tax-efficiency stress test, exploring tailored wealth creation strategies is a wise first step toward clarity.

Asset Ownership and Tax Structures

The way you own an asset is often just as important as the asset itself. Holding investments in your personal name might be simple, but it could expose you to higher marginal tax rates as your income grows. If you use structures like a Family Trust or a Self-Managed Super Fund (SMSF), you may find opportunities to distribute income more efficiently or access lower tax rates. Choosing the right structure early on can significantly reduce your effective tax rate and simplify your estate planning. It’s about building with the end in mind, ensuring your wealth can eventually transition to the next generation without unnecessary hurdles.

Retirement Planning: The Ultimate Integration Test

The transition from the accumulation phase to the income phase is where your financial roadmap is truly tested. Without a coordinated plan, you might face “tax shocks” when you start drawing down on your hard-earned savings. Successful retirement planning requires your Superannuation to work in perfect harmony with your non-Super assets. If you can align these different income streams, you can create a tax-effective lifestyle that lasts as long as you do. This level of integration provides the peace of mind that comes from knowing your future is secure and your strategy is sound.

Maximising Outcomes: Siloed vs. Integrated Wealth Management

If you have ever experienced the frantic rush of the ‘June scramble’, you know how stressful reactive financial decisions can be. Many Australians treat their tax return as an isolated event, separate from their investment journey. However, integrating tax planning with wealth management allows you to replace that last-minute panic with a calm, year-round strategy. Instead of looking back at what happened, you are looking forward at what is possible. This shift from a reactive to a proactive mindset is what distinguishes a well-stewarded portfolio from one that is merely surviving.

Coordinated Capital Gains Tax (CGT) management is a prime example of this integrated approach. When your wealth manager and tax specialist work as one, they can time the sale of assets to coincide with years where your marginal tax rate might be lower, or when you have offsetting losses available. This level of precision can significantly improve your portfolio’s net return. It ensures more of your wealth remains where it belongs: helping you achieve your personal milestones. By viewing tax as a constant variable rather than a year-end hurdle, you gain a level of control that siloed advice simply cannot offer.

Managing Capital Gains and Franking Credits

Australian investors have a unique advantage through franking credits. These credits represent the tax a company has already paid on its profits before distributing them to you as dividends. In a managed strategy, we ensure these credits are utilised to their full potential, often boosting retirement income or offsetting other tax liabilities. Franking credits act as a tax-paid dividend for Australian shareholders. By strategically timing asset sales and understanding the flow of these credits, you can make the most of available offsets and ensure your income streams are as efficient as possible.

Professional Tax Return Preparation as a Strategic Tool

Most people view tax return preparation as a mere compliance hurdle; a box to be ticked once a year. In an integrated model, it becomes the final piece of the strategic puzzle. When your wealth manager handles your tax return, there is no loss of information between professionals. They already understand the ‘why’ behind every transaction and the long-term goal of every structure.

Having your financial data under one roof offers several benefits:

- Clarity: You receive a unified view of your progress without needing to reconcile fragmented reports.

- Accuracy: Your filing is backed by the same professionals who executed the strategy, reducing the risk of errors.

- Integrity: It ensures that your annual compliance actually supports, rather than contradicts, your long-term wealth plan.

This coordinated filing protects the integrity of your wealth creation journey. It provides a level of clarity that makes complex decisions feel manageable and gives you the confidence that your financial house is in order.

The Mentorship Factor: Why a Trusted Guide Matters

While technology has made it easier to track investment balances, it has yet to replicate the wisdom of a human partner. A robo-advisor can calculate a risk profile, but it cannot sit across the table from you to discuss the legacy you wish to leave for your grandchildren. By integrating tax planning with wealth management, a professional mentor does more than just manage assets; they provide a steady hand during periods of market volatility. This human connection is what transforms a collection of financial products into a resilient life strategy.

Many investors wonder if they could simply manage their affairs themselves or rely on automated platforms. While DIY management is possible, it often lacks the objective discipline required when markets turn red. A mentor acts as a buffer against emotional decision-making, ensuring that a temporary dip in the market doesn’t lead to a permanent loss of capital. This professional stewardship provides a level of peace of mind that allows you to focus on your life, rather than the daily fluctuations of the ASX.

Beyond the Balance Sheet: Understanding Your ‘Why’

A professional consultation is designed to uncover the goals that numbers alone cannot show. Are you planning for an early retirement to spend more time with family, or are you looking to fund a specific philanthropic endeavour? These aspirations are the true drivers of your financial roadmap. As your family dynamics and personal ambitions evolve, your mentor ensures your plan remains flexible. This process provides validation and support during major life transitions, helping you navigate the emotional nuances of change with quiet confidence.

Transparency and the ROI of Professional Advice

It’s natural to ask, “how much does a financial advisor cost?” when considering professional help. However, the more important question is often about the value received. The “Advice Gap” refers to the measurable difference between those who plan and those who don’t. In many cases, professional planning pays for itself through the identification of significant tax savings and the avoidance of costly structural errors. Transparency in fees is the hallmark of a professional mentor; you should always know exactly what you are paying and the specific value being delivered in return. If you are ready to move beyond fragmented reports and gain a unified view of your future, reaching out for professional financial advice is a proactive step toward lasting stability. For those with complex family trusts, multiple properties, and sophisticated superannuation strategies, understanding how to choose and work with a private wealth advisor in Australia can help you find the right dedicated steward for your family’s future.

Securing Your Future with Financial Mentors Wealth Management

When you look back on your financial journey, you want to see a story of steady progress rather than a series of disconnected decisions. At Financial Mentors Wealth Management, led by Murray Frean, we have spent years helping Australians turn complex financial puzzles into clear, actionable roadmaps. Our firm was built on the belief that professional financial advice should be a partnership. We don’t just provide reports; we act as a trusted guide to help you navigate the milestones of life with confidence and clarity.

Our approach is built upon three integrated pillars: Tax, Retirement, and Wealth. We have found that true stability only comes when these areas work in harmony. By integrating tax planning with wealth management, we ensure that your investment strategy is always supported by efficient tax structures. This holistic view is backed by our independent Australian Financial Services Licence, held through Financial Mentors AFSL Pty Ltd. This independence is a vital benchmark of professional standards; it means our focus remains entirely on your long-term well-being and the stewardship of your family’s assets.

Our Approach to Tailored Financial Roadmaps

The Australian financial landscape is often filled with dense jargon and intimidating technical terms. We believe our role is to translate these complex laws into plain English, so you always feel in control of your choices. If you understand the “why” behind a strategy, you are more likely to stay the course during market cycles. We prioritise your peace of mind by building strategies that are as practical as they are wise. This partnership approach means we are with you every step of the way, from the early years of wealth creation to the eventual transition into a secure retirement.

Ready to Start Your Journey?

If you are tired of managing fragmented accounts and feeling like your financial life lacks a centre, it might be time for a different conversation. Moving from a disjointed collection of investments to a unified plan is simpler than you might think. In your first meeting with a Financial Mentors advisor, we focus on listening. We want to understand your aspirations, your challenges, and what a secure legacy looks like for you. There is no high-pressure sales pitch; just an honest discussion about where you are and where you want to be.

We invite you to take the first step toward a simplified financial life. By integrating tax planning with wealth management, you can stop reacting to tax time and start looking forward to your future. If you are ready to experience the quiet confidence that comes from being prepared, we are here to help you begin. Secure your financial future with a tailored plan from Financial Mentors Wealth Management.

Your Path to a Unified Financial Future

Moving away from a siloed approach is the first step toward true financial clarity. By integrating tax planning with wealth management, you ensure that every investment decision supports your broader life goals rather than just your year-end balance. We have explored how proactive strategies can replace the stressful ‘June scramble’ and why having a professional mentor provides the discipline needed to navigate market shifts with quiet confidence.

Since 2003, Financial Mentors Wealth Management has operated under our own independent AFSL, providing the steady guidance Australian families need to protect their legacy. Whether you require specialised expertise in retirement and estate planning or simply want the ease of integrated tax return preparation, our team is here to support your journey. If you’re ready to move from fragmented accounts to a unified roadmap, it is time for a meaningful conversation. We invite you to organise a consultation with Financial Mentors Wealth Management and take the next step toward lasting peace of mind. Your future is worth the preparation, and we look forward to walking that path with you.

Frequently Asked Questions

What is the difference between a financial planner and a wealth manager?

Wealth management is a more comprehensive approach that coordinates your total financial ecosystem, including investments, tax, and estate planning. While a financial planner might focus on specific areas like superannuation or insurance, a wealth manager acts as a steward for your entire journey. This ensures every decision you make is aligned with your long-term life milestones and family aspirations.

How does integrating tax planning improve my investment returns?

Integrating tax planning with wealth management improves your returns by focusing on what you actually keep after tax rather than just the gross gains. By timing capital gains, utilising franking credits, and choosing the right ownership structures, you reduce the amount of wealth lost to avoidable taxes. It’s about making your money work harder through precision and foresight, ensuring your portfolio remains efficient as laws evolve.

Do I need to be ultra-wealthy to use wealth management services?

You don’t need to be ultra-wealthy to benefit from professional stewardship. If you have a family, own assets, or are planning for retirement, an integrated strategy can simplify your life and protect your future. It’s particularly valuable for those who find the complexity of Division 293 or Superannuation laws stressful and want a clear, unified roadmap to guide their decisions.

Can a wealth manager help with my annual tax return preparation?

Yes, a comprehensive wealth manager can handle your annual tax return preparation to ensure your strategy and compliance are perfectly aligned. This “under one roof” approach means your tax filing accurately reflects your investment goals and long-term strategy. It removes the frustration of miscommunication between separate professionals and provides you with a single, trusted point of contact for your financial life.

What is an AFSL and why does it matter for my financial security?

An AFSL is an Australian Financial Services Licence, which is a legal requirement for providing professional financial advice in Australia. It matters because it ensures your advisor is regulated by ASIC and adheres to strict ethical and professional standards designed to protect you. Choosing a firm with its own licence, like Financial Mentors, provides a benchmark of quality and security for the management of your assets.

How often should my integrated wealth and tax plan be reviewed?

You should review your integrated plan at least once a year to account for changes in Australian tax laws or your personal circumstances. Major life transitions, such as starting a family, changing careers, or entering retirement, also warrant a strategic review. Regular check-ins ensure your financial roadmap remains relevant and continues to protect your family’s stability through every stage of life.

Is estate planning included in wealth management services?

Estate planning advice is a core part of wealth management because it focuses on the long-term stewardship of your legacy. While we don’t draft the legal documents ourselves, we provide the strategic advice needed to ensure your assets are distributed according to your wishes. This coordination helps avoid unnecessary tax burdens for your heirs and provides the peace of mind that comes from being prepared.

How much do financial advisors typically charge in Australia?

Financial advisor fees in Australia vary depending on the complexity of your situation and the level of ongoing support you require. Most professional mentors use a transparent fee structure, which might include a flat fee for a statement of advice or a fee based on the services provided. The focus should always be on the value and potential tax savings the advice delivers rather than just the initial cost. If your financial situation has grown in complexity, learning more about how to choose and work with a private wealth advisor can help you evaluate whether a more specialised level of professional stewardship is right for you.