What if the “million dollar” retirement target you’ve been told to aim for is actually a myth that’s causing you unnecessary stress? If you’ve been searching for a definitive answer on how much do i need to retire in australia, you’ve likely encountered a sea of conflicting numbers and complex jargon. It’s natural to feel concerned that inflation might erode your nest egg or that you’ll inadvertently fall foul of the latest Age Pension asset limits. We understand that this isn’t just about spreadsheets; it’s about the peace of mind that comes from knowing you’re prepared for the next chapter of your life.

This 2026 guide is here to provide the supportive clarity you deserve. We’ll help you understand the updated ASFA “comfortable” benchmarks, which currently sit at A$630,000 for singles and A$730,000 for couples, while explaining how these figures interact with your specific lifestyle goals. If you want to ensure your future is stable, then reviewing the new July 2026 pension thresholds and income tests is a vital first step. We will show you how to calculate a personal retirement number that secures both your daily comforts and the legacy you wish to leave behind.

Key Takeaways

- Identify the latest 2026 benchmarks for a “comfortable” retirement to ensure your plan covers essential healthcare, travel, and social connection.

- Discover how to calculate a personal target for how much do i need to retire in australia that reflects your actual lifestyle rather than generic industry myths.

- Learn how to navigate the updated 2026 Age Pension asset and income tests to maximise your entitlements alongside your superannuation.

- Understand the importance of a bespoke strategy that manages complex dynamics like estate planning for blended families and tax-effective income streams.

- Gain peace of mind by shifting from a “nest egg” mindset to a sustainable “life income” strategy with the support of a professional mentor.

The 2026 Retirement Benchmarks: What Does a “Comfortable” Lifestyle Cost?

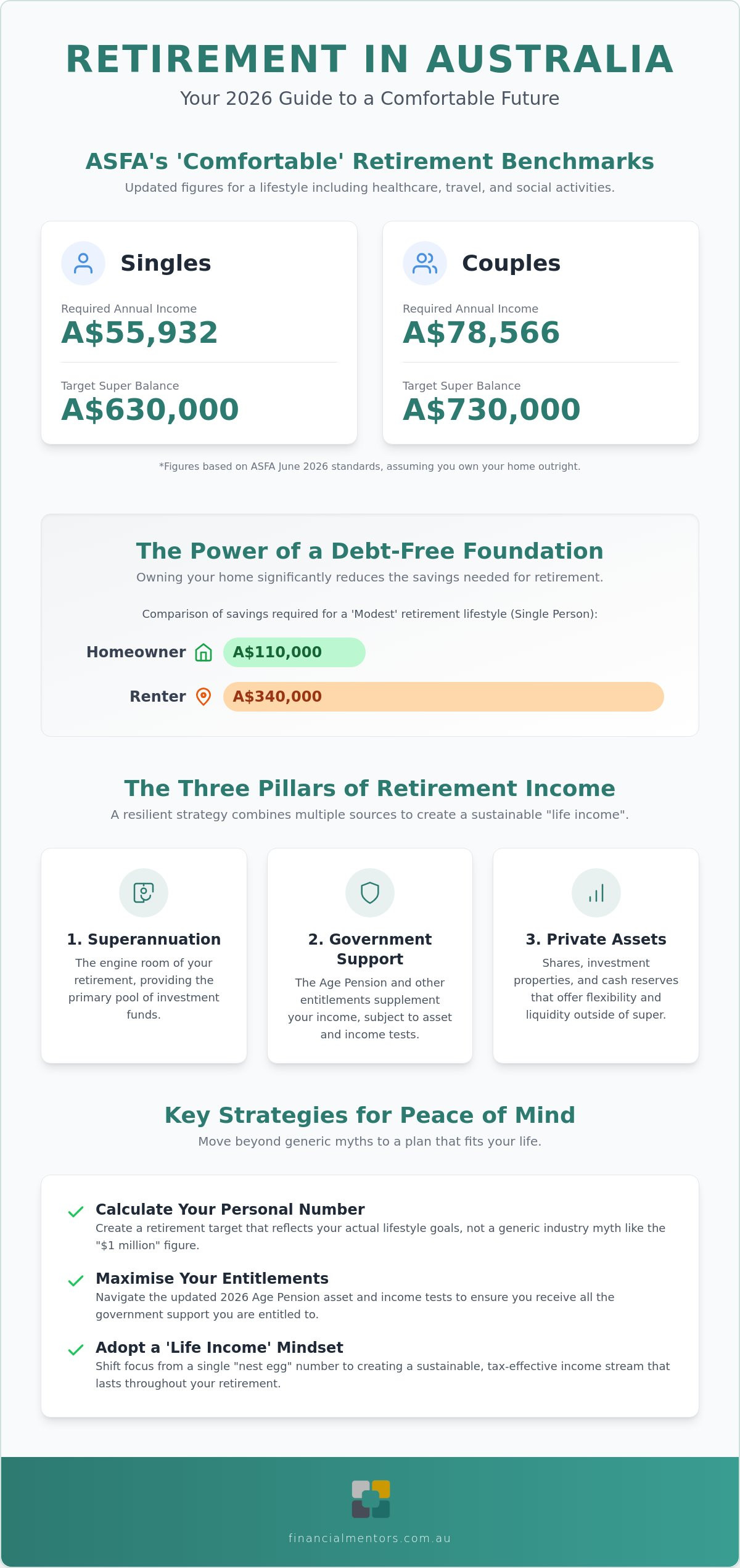

Setting a retirement goal often starts with a single, daunting question: how much do i need to retire in australia? While the answer is deeply personal, the Association of Superannuation Funds of Australia (ASFA) provides a helpful starting point through their quarterly standards. As of June 2026, the “comfortable” standard suggests an annual income of A$55,932 for singles and A$78,566 for couples. These aren’t just arbitrary figures. They represent the ability to maintain a lifestyle that includes private health insurance, regular travel, and the freedom to stay connected with your community. If you’ve spent your career in a professional role, you’ll likely find that the “modest” standard, which covers only the basics, feels far too restrictive for the retirement you’ve imagined.

Understanding the foundation of Superannuation in Australia is key to seeing these benchmarks as a compass rather than a rigid rule. The system is designed to provide a base level of support, but your unique aspirations determine the true target. Think of these benchmarks as a guide to help you navigate the sea of information. They allow you to adjust your sails based on whether you want to spend your time caravanning around the coast or enjoying city theatre nights. We believe in validating your specific dreams, ensuring your plan reflects your life, not just a statistic.

Breaking Down the 2026 Expenditure

Inflation has shifted what “comfortable” looks like in 2026. Healthcare remains a significant factor; many retirees now account for rising private health insurance premiums and the “gap” payments for specialists that have increased over the last year. Beyond health, your budget now needs to accommodate digital essentials. High-speed internet and smart home technology aren’t luxuries anymore. They’re the tools that keep you connected to family and help you manage your home efficiently as you age. A truly comfortable budget ensures you don’t have to choose between upgrading your home security, investing in a whole home water filtration system installation australia, or a weekend away with friends.

The Importance of a Debt-Free Foundation

Your home is perhaps the most critical piece of your retirement puzzle. The ASFA benchmarks assume you own your home outright. If you’re entering retirement with a mortgage, your required savings will be significantly higher to cover those ongoing repayments. In fact, for a modest retirement, a single renter currently needs approximately A$340,000 in savings, compared to just A$110,000 for a homeowner. Many people find peace of mind by using a portion of their superannuation to clear remaining debts before they finish work. This strategy reduces monthly stress and aligns with the July 2026 Age Pension rules, where your primary residence is generally exempt from the asset test, making home ownership a powerful pillar for long-term stability.

Reducing fixed overheads is another key part of financial stewardship for homeowners. In Western Australia, many retirees find that solar panel installation Perth—often combined with modern battery storage—provides a practical way to lower electricity bills, ensuring more of their superannuation can be spent on lifestyle rather than utility costs.

The Three Pillars of Retirement Income: Beyond Your Super Balance

Many people fixate on a single, daunting figure when asking how much do i need to retire in australia. However, a truly resilient strategy relies on three distinct pillars: superannuation, government support, and your private assets. Balancing these elements effectively is what transforms a simple savings account into a sustainable stream of “life income.” It’s about looking at your financial world as a whole rather than a series of disconnected parts. When these pillars are aligned, you gain the confidence to move forward without the constant worry of running out of funds.

Your private investments, such as shares, investment properties, or cash reserves, play a vital role in providing flexibility. These assets often sit outside the superannuation environment, offering a different layer of liquidity. If you have a diversified portfolio, you can better manage market fluctuations and inflationary pressures. Integrated tax planning ensures that the income generated from these sources is structured efficiently. By coordinating your retirement planning with professional tax return preparation, you can identify opportunities to preserve more of your wealth for your daily needs and your family’s future.

Superannuation and Choice Income

Superannuation remains the engine room of your retirement strategy. For the 2026/2027 financial year, you can potentially boost your balance through concessional contributions up to A$32,500. If you aren’t quite ready to stop work entirely, a Transition to Retirement (TTR) strategy might be the perfect middle ground. It allows you to access a portion of your super while you’re still earning a salary, helping you ease into a new pace of life. Deciding between an account-based pension or a lump-sum withdrawal is a significant milestone. Choosing the right investment mix within your fund ensures your money continues to grow even as you begin to draw upon it.

Strategic Tax and Government Support

The Age Pension is a flexible supplement that can work alongside your superannuation, not just an “all or nothing” benefit. From 1 July 2026, the asset test thresholds have been updated; for example, a single homeowner can now hold up to A$333,000 in assets and still receive the full pension. Navigating the A$2.1 million transfer balance cap requires a steady hand to avoid unnecessary tax penalties. Referring to the ASFA Retirement Standard helps you see how private wealth and government entitlements combine to meet your desired lifestyle. If you structure your assets thoughtfully, you can often maximise your pension eligibility while maintaining a comfortable lifestyle.

Debunking the $1 Million Myth: Why Your “Number” is Personal

Have you ever felt a pang of anxiety when seeing headlines claiming you need at least a million dollars to stop work? This “seven-figure myth” often does more harm than good, leading many people to feel they’ll never reach the finish line. The truth is that when you ask how much do i need to retire in australia, the answer is rarely a round, intimidating number. It’s actually a calculation of your personal “burn rate”, which is the amount you specifically need to fund the life you’ve envisioned. By focusing on your actual lifestyle aspirations rather than a generic target, you can reduce stress and gain a clearer sense of direction. Your number is as unique as your fingerprint.

A trusted guide helps you look beyond the balance on your super statement to find “invisible” assets you might have overlooked. These could include home equity, the ability to downsize in the future, or even the capacity to consult part-time in a field you enjoy. While the final sum is a helpful benchmark, the power of compounding remains your greatest ally. Starting your plan today, regardless of your current balance, allows time to do the heavy lifting for you. It’s about progress, not perfection.

The Average vs. The Ideal

It’s helpful to look at where your peers stand to gain some perspective. Data from APRA indicates that the average superannuation balance for Australians aged 65-69 sits between A$430,000 and A$460,000. If your balance is closer to this average than the ASFA “comfortable” targets mentioned earlier, you’re certainly not alone. Bridging this gap is often a matter of making small, deliberate adjustments now. Whether you’re navigating retirement as a single person or as a couple, your strategy should be built on your actual circumstances rather than an industry average that doesn’t know your story.

Stewardship and Future-Proofing

We encourage you to move from a “savings” mindset to one of “stewardship.” Stewardship is the wise, long-term management of your resources to ensure they serve you and your family well throughout your entire retirement. The first five years after you stop working are often the most critical for managing market volatility. Having a steady hand to guide your asset organisation during this period can prevent a temporary market dip from impacting your long-term security. By structuring your wealth thoughtfully, you can create a future-proof plan where you can enjoy your life without the constant fear of outliving your money.

Factoring in Complexity: When Simple Calculators Fall Short

Online tools often provide a generic answer to how much do i need to retire in australia, but they rarely account for the beautiful complexity of real life. If you’re part of a blended family, for instance, your financial roadmap needs to be far more nuanced than a standard spreadsheet can handle. Balancing the needs of a current partner with the legacy you wish to leave for children from a previous relationship requires a thoughtful, human touch. It’s about more than just numbers; it’s about harmony and clear communication across generations. We understand that these emotional nuances deserve as much attention as your bank balance.

Similarly, if you’ve chosen to manage your own retirement through a Self-Managed Super Fund (SMSF), you’ve likely discovered that the increased control comes with a significant workload and higher compliance costs. A health change or the sudden need for aged care can also shift your financial requirements overnight. These aren’t just “what-ifs”; they’re life events that require a flexible strategy. A wise mentor looks at these variables as a whole, helping you adjust your sails when the wind changes direction. This holistic view ensures that your plan remains robust even when life takes an unexpected turn.

Estate Planning and Legacy Protection

Many people believe that having a Will is enough to secure their legacy. In reality, a Will is only one piece of a much larger puzzle. Did you know that your superannuation doesn’t automatically form part of your estate? Without a valid binding death benefit nomination, your hard-earned savings might not end up where you intended. There are also specific tax implications for adult children receiving superannuation death benefits that can be managed with the right estate planning advice. We focus on ensuring your assets are distributed according to your wishes, providing you with the quiet confidence that your loved ones are protected.

The Cost of “Doing it Yourself”

While it’s tempting to try and save on fees by managing everything yourself, the cost of missed opportunities can be far higher. “Cheap” advice often leads to expensive mistakes, particularly when it comes to tax-effective structuring or missing out on government entitlements. Professional financial planning standards provide a level of rigour that DIY methods simply can’t match. It’s about the peace of mind that comes from knowing every stone has been turned. If you want to ensure your strategy is truly future-proof, then investing in professional guidance is often the most practical decision you can make for your long-term stability.

Designing Your New Chapter with Financial Mentors

Retirement isn’t a static destination on a map; it’s a dynamic transition into a new way of living. While we’ve explored the latest benchmarks and the “three pillars” of income, the most important element is often the guidance you receive as you make these life-changing decisions. At **Financial Mentors Wealth Management**, our “Wise Mentor” approach is designed to validate your unique goals and reduce the weight of complex decision-making. We believe that financial advice should feel like a partnership, providing you with the quiet confidence to step into your new chapter with a clear sense of purpose. It’s about turning a superannuation balance into a sustainable life income that respects your history and secures your legacy.

By bringing together strategic Retirement Planning and professional Tax Return Preparation, we ensure that your strategy is as efficient as it is inspiring. This integrated approach means you don’t have to worry about the gaps between your investments and your obligations to the ATO. We help you navigate national regulations and AFSL standards with confidence, ensuring every decision is grounded in practical wisdom and forward-looking stability. When your tax and retirement strategies are aligned, you keep more of your hard-earned wealth working for you and your family.

A Partnership in Stewardship

What can you expect when you sit down for an initial consultation? We start by focusing on your “why” rather than just your “how much.” We might ask how you imagine spending your Tuesday afternoons or what kind of support you’d like to provide for your grandchildren. This focus on purpose allows us to build a flexible roadmap that grows with you through every life transition. The unquantifiable return on investment here isn’t just a number on a screen; it’s the profound peace of mind that comes from knowing your family’s future is future-proofed. We treat your wealth with the same care and stewardship that you’ve applied to earning it over a lifetime.

Taking the Next Step

If you’ve been wondering how much do i need to retire in australia, the best time to seek clarity is today. Your current asset level shouldn’t be a barrier to seeking professional mentorship; in fact, the sooner you start, the more time you have to let compounding work in your favour. We are committed to transparency and provide fee-for-service clarity so you always know exactly where you stand. There is no pressure or urgency, only a methodical and calm dialogue about your future stability. We invite you to take that first step toward a retirement that is as organised as it is rewarding.

Book a reassuring conversation with our retirement planning team

Securing Your Future with Confidence and Clarity

Retirement is one of life’s most significant milestones; it’s a transition that deserves more than just a generic spreadsheet. We’ve seen that while the 2026 ASFA benchmarks provide a useful compass, the true answer to how much do i need to retire in australia is found in your personal aspirations and family dynamics. Whether you’re navigating the updated Age Pension asset tests or structuring a complex estate, the goal is always the same: achieving the peace of mind that comes from being truly prepared.

With over 20 years of associated history and operating under a professional AFSL license, our team is here to act as your trusted guide. We bring together specialised retirement planning, estate advice, and integrated tax return preparation to ensure your wealth is managed holistically. If you’re ready to move past the anxiety of conflicting numbers and start designing a bespoke strategy, we’re here to help.

Book a reassuring conversation with our retirement planning team

Your future stability is within reach, and with a steady hand to guide you, you can look forward to your next chapter with quiet confidence.

Frequently Asked Questions

Is the cost of financial advice tax-deductible in Australia?

The cost of ongoing financial advice is generally tax-deductible if it’s used to manage investments that produce assessable income. However, the fee for the initial plan or Statement of Advice is typically treated as a capital expense and isn’t deductible. if a portion of the fee specifically relates to professional tax return preparation or tax-related advice, that specific part might be claimable. It’s always best to check with a tax professional to see how these rules apply to your unique situation.

Can I pay for my financial planning fees out of my superannuation fund?

You can often pay for advice related to your superannuation directly from your fund’s balance. This is common for advice concerning investment choices or contribution strategies within that specific fund. It’s a practical way to manage your cash flow while ensuring your retirement strategy is professionally guided. Your fund will need to ensure the payment meets the “sole purpose test” before they can process the fee on your behalf.

What is the average cost of a Statement of Advice (SoA) in 2026?

The cost of a Statement of Advice in 2026 varies based on the complexity of your financial situation and the level of strategy required. Industry reports suggest that fees reflect the time and expertise needed to navigate 2026 regulations and personal goals. Instead of looking for the cheapest price, many Australians find value in a fee-for-service model that prioritises transparency. This ensures you understand exactly what you’re paying for before any work begins on your roadmap.

Do I need a certain amount of money to justify the cost of a financial adviser?

There’s no magic number required to justify seeking professional mentorship. If you find yourself asking how much do i need to retire in australia and feeling overwhelmed by the options, the value of a clear plan often far exceeds the cost. Advice is about more than just managing a balance; it’s about reducing stress and making sure you don’t miss out on government entitlements or tax-effective structures that could save you thousands over the long term.

How do I know if the fees I am being quoted are fair and reasonable?

You can determine if a quote is reasonable by looking for a clear, transparent breakdown of the services provided. A professional guide will be happy to explain their fee structure and how it aligns with the value they provide to your specific journey. If a quote feels vague or includes hidden commissions, it’s a good idea to ask for more detail. Focus on the quality of the strategy and the peace of mind it offers rather than the price alone.

What is the difference between an independent and a restricted financial adviser?

An independent adviser must meet strict legal criteria, meaning they don’t receive commissions or have ownership links to financial product issuers. Restricted or “aligned” advisers may be limited to recommending products from a specific list or may have ties to a bank or insurance company. Understanding these relationships helps you see if the advice is truly bespoke or if it’s influenced by external corporate structures.

Can I get a one-off retirement plan without signing up for an ongoing fee?

You can certainly request a one-off retirement plan without committing to an ongoing service agreement. This is often referred to as “project-based” advice and provides you with a comprehensive Statement of Advice to implement at your own pace. While ongoing support helps you adjust to market changes, a one-off plan is a great way to gain a clear starting point if you prefer to manage the day-to-day details yourself.

What happens to my retirement plan if I want to cancel my ongoing service agreement?

If you decide to cancel an ongoing service agreement, your retirement plan remains your property. You’ll still have the strategy we’ve built together, but you’ll take over the responsibility for monitoring market volatility and regulatory changes. We believe in providing you with the tools to succeed, so if your circumstances change and you choose to move on, we’ll ensure the transition is handled with the same respect and care as our initial partnership.