What if you could reclaim your Fridays and start easing into your next chapter without the fear of your bank balance taking a hit? It’s a common worry for many of us as we reach our 60th birthday. You’ve worked hard for decades, and while you might be ready to step back from the high-pressure daily grind, the confusion over complex tax rules and the stress of potentially running out of superannuation can feel overwhelming. Finding the right transition to retirement strategy australia offers can feel like a puzzle, but it’s actually a powerful way to bridge the gap between your career and your future.

With the cost of a comfortable retirement in 2026 now reaching $78,566 per year for couples, we understand that you want to protect your lifestyle while ensuring your superannuation continues to grow. This guide will show you how to use a TTR income stream to reduce your working hours or pay less tax on your salary, helping you reach your goals with a larger balance. We’ll walk through the current rules, such as the 4% minimum drawdown, and show you how a steady plan can provide the peace of mind you deserve.

Key Takeaways

- Learn how to access your superannuation while you are still in the workforce, creating a gentle bridge between your full-time career and your future leisure.

- Discover how a transition to retirement strategy australia allows you to either work fewer days each week or significantly boost your super balance before you finish up.

- Understand the specific rules regarding preservation age and withdrawal limits to ensure your plan remains compliant and effective.

- Explore why it is vital to look at the impact on your wealth at age 80, not just your immediate lifestyle, when deciding if this path is right for you.

- See how professional retirement planning advice can help you organise the complex tax and super rules into a clear, supportive roadmap for your next chapter.

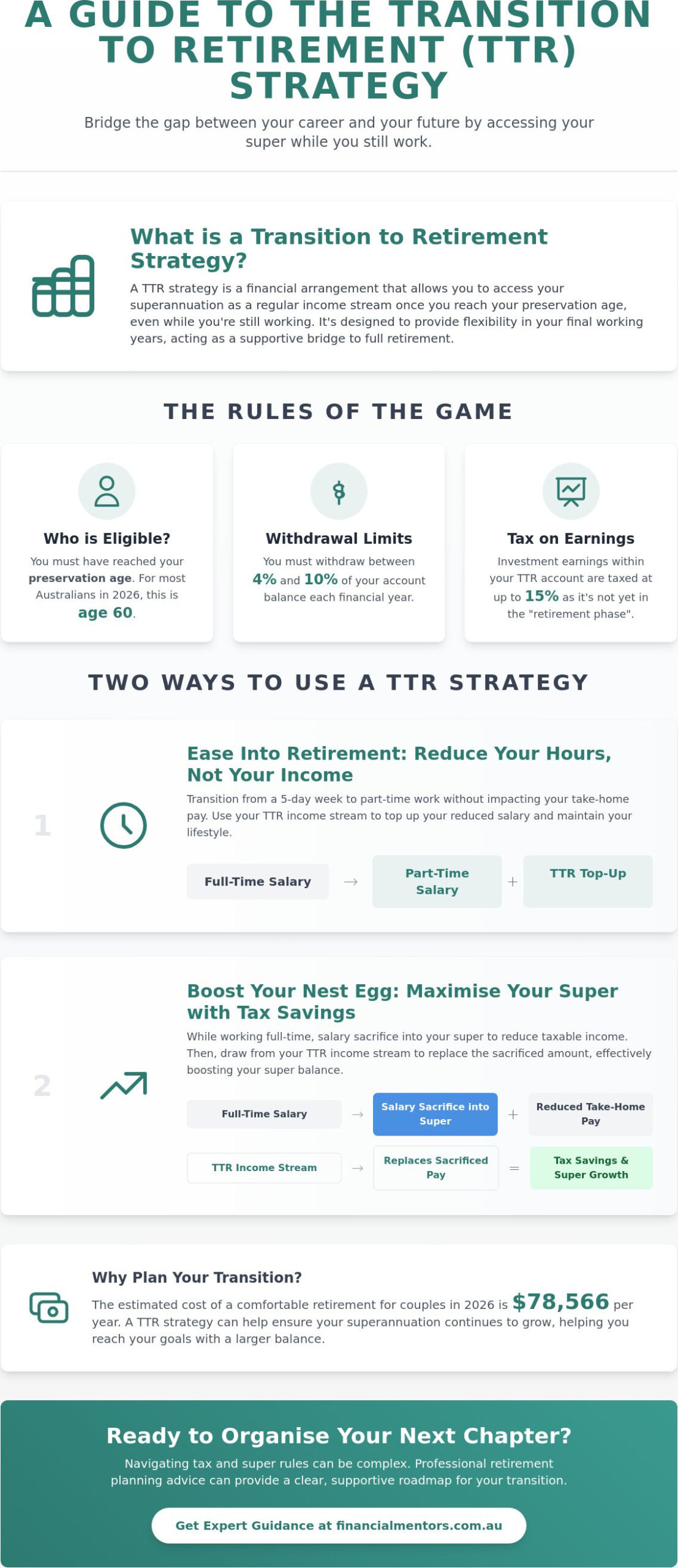

What is a Transition to Retirement (TTR) Strategy?

A transition to retirement strategy australia is a specific financial arrangement designed for workers aged 60 and over in 2026 to access their superannuation while remaining in the workforce. If you have reached your preservation age but aren’t quite ready to hang up the boots, this strategy acts as a bridge between your full-time career and your future leisure. It isn’t an “all or nothing” choice; rather, it’s a way to customise your final working years to suit your personal needs.

The primary goal of this approach is to give you flexibility. For some, that means the freedom to work fewer days without seeing a drop in their take-home pay. For others, it’s a powerful tool to build a larger nest egg by taking advantage of tax incentives. By starting a TTR income stream (TTRIS) alongside your regular employment income, you can choose a path that feels right for your unique circumstances.

The Core Concept: Accessing Super While Working

How does this work in practice? Essentially, you can draw a regular pension payment from your super balance while you continue to receive a salary from your employer. You don’t need to retire, resign, or even change your current job to start. This dual income allows you to maintain your current lifestyle even if you decide to reduce your hours to part-time. It’s a supportive way to test the waters of retirement before making a permanent commitment.

Many Australians also use this strategy to “recycle” their income. If you stay in full-time work, you might choose to salary sacrifice a portion of your pay into your super fund to reduce your taxable income. You can then replace that reduced salary with payments from your TTR income stream. This method often results in paying less tax overall, allowing more of your hard-earned money to stay within your super environment where it can continue to grow.

Who is Eligible for TTR in 2026?

Eligibility for this strategy is tied closely to your preservation age. As of 2026, the preservation age for most Australians is 60. This is the official age at which you can begin to access the funds held within the system of Superannuation in Australia, provided you use a transition to retirement income stream. If you haven’t reached 60, you generally cannot access these funds while you are still working.

It’s important to recognise that a TTR income stream is different from a standard retirement pension. Because you are still working, your TTR account is not yet in the “retirement phase.” This means the investment earnings on the assets in your TTR account are still taxed at a rate of up to 15%. Additionally, the government sets strict limits on how much you can withdraw. You must take at least 4% of your balance each financial year, but you are capped at a maximum of 10%. These rules ensure the strategy is used as a steady transition tool rather than a way to withdraw your entire balance at once.

Two Ways to Use TTR: Easing into Leisure or Boosting Your Nest Egg

How do you picture your final years in the workforce? Perhaps you are looking for a way to reclaim your Fridays, or maybe you’re determined to make every dollar work harder before you finish up. The beauty of a transition to retirement strategy australia is that it acts as a versatile multi-tool for your finances. It doesn’t force you into a single box. Instead, it adapts to your specific needs. Ultimately, the right path for you depends on your personal wealth goals and how you value your time versus your future balance.

Option 1: Reducing Your Working Hours

For many Australians, the jump from a high-pressure, five-day week to total retirement can be a significant emotional shock. Have you considered what it would feel like to transition slowly? By moving to a three or four-day week, you can ease into your next chapter while using your superannuation to “top up” your reduced salary. This ensures your household budget stays steady even as your leisure time increases.

This approach offers a wonderful opportunity to test the waters. It allows you to discover how you’ll actually spend your time without the stress of a permanent commitment. If you find you’re not quite ready for so much free time, you haven’t fully retired, so you maintain your professional connections. It’s about finding a balance that supports your mental well-being as much as your wallet. To get a better sense of the mechanics, it’s helpful to understand What is a Transition to Retirement (TTR) Strategy? and how it fits your lifestyle.

Option 2: The Tax-Effective “Boost” Strategy

If you aren’t ready to reduce your hours just yet, you can use a transition to retirement strategy australia purely as a wealth creation tool. This involves a clever synergy between salary sacrifice and your TTR income stream. By contributing more of your pre-tax salary into super, you effectively lower your taxable income. You then replace that missing take-home pay with payments from your super account.

If you are aged 60 or over, these pension payments are generally tax-free. This means you are essentially moving money from a higher-tax environment (your salary) into a lower-tax environment (your super, where concessional contributions are taxed at just 15%). Over a few years, this strategy can significantly increase your final balance without you having to change your daily spending habits. If you’re feeling unsure about which direction to take, speaking with a retirement planning specialist can help you organise these moving parts into a clear roadmap.

The Rules of the Game: Navigating Preservation Age and Limits

While the freedom of a transition to retirement strategy australia is appealing, it’s vital to remember that this path operates within a structured framework. The Australian government sets strict parameters to ensure these strategies are used for their intended purpose: providing a steady bridge to your future rather than a quick way to empty your nest egg. In 2026, the most significant milestone for most of us is reaching the preservation age of 60. This is the age when the doors to your superannuation begin to open, but they don’t open all the way just yet.

Success with this strategy requires a bit of annual housekeeping. Because the rules involve specific percentages and tax thresholds, staying organised is the best way to maintain your peace of mind. If you don’t meet the mandatory requirements, you could face unexpected tax consequences; so it’s always wise to review your plan at the start of each financial year. It’s a delicate balance to get right, but the rewards for your lifestyle can be significant.

The 4% to 10% Withdrawal Rule

One of the most important constraints involves how much money you can actually take out of your TTR account. Unlike a standard retirement pension where you can often withdraw as much as you like once you’ve fully retired, a TTR account has a strict 10% maximum withdrawal cap on the account balance each financial year. This ensures that your super continues to provide for you throughout your 70s, 80s, and beyond. At the same time, you must withdraw a minimum of 4% of your balance annually.

- Balance calculation: Your minimum and maximum amounts are calculated based on your account balance on 1 July each year.

- Mandatory payments: You must ensure at least the 4% minimum is paid out by 30 June.

- The 10% limit: You cannot exceed this cap, even if you have an unexpected expense.

Tax on TTR Income: Before and After 60

The way your pension payments are treated by the tax office changes dramatically once you celebrate your 60th birthday. If you are aged 60 and over, your TTR pension payments are generally tax-free. This is a significant advantage that allows you to keep more of your money in your pocket. For those who may have reached their preservation age before turning 60, the taxable portion of their payments is taxed at their marginal rate, though they usually receive a 15% tax offset to help soften the blow.

You should also be aware of the General Transfer Balance Cap, which is $2.1 million as of 1 July 2026. This cap limits the total amount of super you can move into a tax-free retirement pension. While TTR accounts are technically not in the retirement phase yet, understanding how this cap will affect you once you eventually retire or turn 65 is a key part of being prepared. It’s all about looking ahead to ensure your strategy remains practical for the long term.

Is a TTR Strategy Right for Your Circumstances?

While the mechanics of a transition to retirement strategy australia are quite structured, the decision to start one is deeply personal. It isn’t a one size fits all solution that every Australian should adopt the moment they turn 60. Instead, it’s a choice that requires you to look honestly at your current needs and your long-term aspirations. Have you considered how your lifestyle choices today might impact your total super balance when you are 80, rather than just when you hit 65? It’s also vital to consider your partner’s financial position, as a strategy that works for you might change the tax or benefit outcomes for your household as a whole.

One often overlooked aspect is how accessing your super early might affect other entitlements. For example, if you are approaching the age where you might qualify for the Age Pension, the way your TTR income stream is assessed under the means test could be different from other types of savings. Taking the time to understand these ripples in your financial pond now will help you avoid surprises later on. Working with experienced retirement planners in Australia can help you map out these interactions and ensure your strategy accounts for every moving part.

The Benefits: Why Most Consider TTR

The most immediate drawcard is the ability to maintain your current standard of living while you begin to reclaim your time. If you choose to work fewer days, the pension payments fill the gap in your take-home pay, allowing you to enjoy your hobbies or spend time with family without financial stress. For those staying full-time, the tax savings can be significant. Middle and high-income earners often find that “recycling” their income through salary sacrifice leads to a much lower overall tax bill.

Another major plus is that your employer’s super guarantee contributions don’t stop. Even if you are drawing a pension from one part of your super, your boss will still pay contributions into your accumulation account based on your actual earnings. This helps keep the momentum going in your nest egg even as you start to use some of it.

The Potential Drawbacks and Objections

The main trade-off is the “compounding” cost. Every dollar you withdraw today is a dollar that isn’t sitting in your fund earning investment returns. Over ten or twenty years, those withdrawals can add up, potentially leaving you with a smaller balance in your later years. There’s also an administrative burden to consider. Running a pension account alongside an accumulation account requires careful record-keeping and annual reviews to ensure you stay within the 4% to 10% limits.

You might find yourself asking if the cost of a financial mentor is truly worth the tax savings you might gain. While it’s a valid question, many find that the peace of mind coming from a professionally managed retirement planning roadmap far outweighs the fees. A guide helps you look past the immediate tax wins to ensure your strategy remains sustainable for the next thirty years. It’s about stewardship of your future self, ensuring that the “you” at age 85 is just as well looked after as the “you” today.

Partnering with a Mentor: How Professional Advice Optimises Your Transition

A transition to retirement strategy australia is rarely a simple “set and forget” arrangement. It is a sophisticated financial manoeuvre that requires several moving parts to work in perfect harmony. You have to consider the intersection of tax law, superannuation regulations, and even your specific employment contract. While the numbers on a spreadsheet are important, a financial mentor helps you look beyond the data to see the life you actually want to lead. It is about ensuring that your strategy doesn’t just look good on paper, but feels right for your daily reality.

One of the most significant risks when setting up a TTR plan is accidentally breaching ATO contribution caps. For the 2026 financial year, the concessional contributions cap is $30,000. If you are salary sacrificing heavily to boost your super while also drawing a pension, it is easy to miscalculate and face unexpected penalties. Professional guidance acts as a safety net, ensuring you stay within the rules while maximising your tax efficiency. Often, the value found in these tax savings and the avoidance of costly mistakes far outweighs the advisor fees. It is an investment in stewardship that protects your hard-earned wealth. Partnering with dedicated retirement planners who understand the nuances of TTR strategies can make the difference between a plan that merely works and one that truly thrives.

Tailoring the Strategy to Your Life Goals

Why settle for a generic online calculator when your life is anything but average? A calculator can tell you a projected balance, but it cannot tell you how a transition to retirement strategy australia fits with your estate planning wishes or your specific wealth creation goals. At Financial Mentors Wealth Management, we believe in building a personalised roadmap. We look at how your transition affects your entire financial ecosystem, including your spouse’s position and your long-term legacy. This holistic approach ensures every decision you make today supports the person you want to be in twenty years.

Taking the Next Step with Confidence

There is a profound sense of peace that comes from knowing your retirement plan has been “stress-tested” against various life scenarios. If you feel ready to explore these possibilities, the first step is often the most important. Start by having an open conversation with your partner about your ideal work-life balance. Once you have a shared vision, you can then approach your employer to discuss potential flexible working arrangements. If you are ready to see how these pieces fit together for you, we invite you to Organise a consultation with Financial Mentors Wealth Management today. We are here to sit across the table and guide you through each step of the journey with quiet confidence.

Embracing Your Next Chapter with Confidence

Choosing to step back from full-time work doesn’t have to mean stepping away from financial security. By understanding how a transition to retirement strategy australia works, you can find a balance that honours both your current lifestyle and your future needs. Whether you decide to reduce your hours or focus on boosting your super through tax-effective contributions, the key is to remain organised and forward-looking. You’ve worked hard to reach this stage; now it’s time to ensure your wealth is managed with the care it deserves.

At Financial Mentors Wealth Management, we bring over 20 years of experience under AFSL 2003 to every conversation. Our specialist retirement and estate planning advice is delivered with an empathic, mentor-led approach, ensuring you feel supported through every decision. If you are ready to move toward a more flexible future, we are here to help you navigate the path ahead. Start your journey to a secure future with Financial Mentors Wealth Management and discover the peace of mind that comes from being truly prepared. Your best years are still to come.

Frequently Asked Questions

What is the preservation age for a TTR strategy in 2026?

Your preservation age in 2026 is 60 for almost all Australians. If you were born on or after 1 July 1964, you must reach this milestone before you can access your superannuation through a transition to retirement income stream. Reaching this age is a significant milestone that allows you to start planning your next chapter with greater flexibility and confidence.

Can I withdraw my super as a lump sum while using a TTR strategy?

You generally cannot withdraw your super as a lump sum while you are still working and using a TTR account. The rules are designed to provide a steady income bridge, so your withdrawals are capped at a maximum of 10% of your account balance each financial year. Once you reach age 65 or meet another condition of release, these restrictions usually fall away.

How much does a financial advisor cost to set up a TTR strategy?

The cost of professional advice varies depending on the complexity of your financial situation and the specific goals you wish to achieve. We recommend organising a consultation to discuss your personal circumstances; as this allows for a tailored quote that reflects the level of stewardship your transition requires. Many find that the tax efficiencies gained through a transition to retirement strategy australia provide significant value over the long term.

Will a TTR strategy affect my employer’s super contributions?

Starting a TTR strategy does not reduce the superannuation guarantee contributions your employer is legally required to pay. These contributions are calculated based on your ordinary time earnings from your job, regardless of any pension income you receive. This ensures that your nest egg can continue to grow even as you begin to access a portion of your savings to support your lifestyle.

Can I stop a TTR income stream if my circumstances change?

You have the flexibility to stop your TTR income stream at any time if your life situation evolves. If you decide to return to full-time work or find that you no longer require the additional income, you can commute the pension back into a standard accumulation account. This adaptability is a reassuring feature that allows you to remain in control of your financial roadmap.

Does a TTR strategy work for self-employed Australians?

A transition to retirement strategy australia is a practical option for self-employed individuals who have reached their preservation age. It can be a wise way to manage your cash flow while you perhaps scale back your business involvement or focus on wealth creation. You can continue to make personal contributions to your super while drawing a pension, provided you stay within the relevant contribution caps.

How does TTR interact with the $30,000 concessional contribution cap?

The TTR strategy works alongside the $30,000 concessional contribution cap by allowing you to salary sacrifice more of your income into super. You then use the pension payments to replace the take-home pay you have contributed. It is vital to ensure that the combined total of your employer contributions and any salary sacrifice remains within this $30,000 limit to avoid any unexpected tax penalties.

Is the income from a TTR account tax-free if I am over 60?

Pension payments from a TTR account are generally tax-free once you reach the age of 60. This is one of the most supportive aspects of the strategy, as it allows you to receive your super income without it being added to your taxable salary. While the investment earnings within the account itself are still taxed at up to 15%, the money that lands in your bank account is typically yours to keep.