If you have spent years diligently building a nest egg for your future, could a change in tax law quietly reshape your retirement plans? Many Australians are currently feeling a mix of confusion and concern as the 1 July 2027 transition date approaches. It’s understandable to feel anxious about how your long-held assets will be treated under the new rules. You’ve worked hard to grow your wealth; it’s only right that you want to protect it from unexpected tax burdens. We believe that clarity is the best antidote to uncertainty, and we’re here to walk you through this transition with steady, professional guidance.

In this guide, we’ll help you understand the move away from the 50% capital gains tax discount australia has utilised for decades toward the new inflation-based indexation model. You’ll learn exactly how the 2026-27 reforms affect your current holdings and whether your assets will benefit from grandfathering provisions. By the end of this article, you will have a clear timeline of the changes and a practical sense of how to organise your wealth creation strategies for the years ahead. Let’s look at how you can navigate these shifts while keeping your long-term goals firmly in sight.

Key Takeaways

- Learn why the 1 July 2027 cutoff is a pivotal date for your investments and how to identify which of your assets are protected by current rules.

- Discover how the shift from the traditional capital gains tax discount australia offers to a new inflation-based calculation might change your final tax bill.

- Understand the vital role of applying your capital losses correctly to ensure you aren’t paying more than your fair share as the reforms take hold.

- Explore how these legislative changes could influence your retirement timeline and the best ways to organise the transfer of assets to the next generation.

- See how moving from simple tax preparation to a holistic wealth creation strategy can help you feel more secure and prepared for the future.

What is the Capital Gains Tax (CGT) Discount in Australia?

When you decide to sell an asset that has grown in value, it is natural to feel a sense of accomplishment. However, that growth also brings a tax responsibility that can feel a bit overwhelming if you aren’t prepared. It is helpful to remember that Capital Gains Tax is not actually a separate tax. Instead, any profit you make from the sale of an asset is included as part of your assessable income for the financial year. The Capital Gains Tax in Australia framework was designed to ensure that wealth growth is treated fairly alongside your regular earnings. To encourage Australians to invest in the nation’s future, the government provides a mechanism to lower the tax burden on assets held for the long term.

The CGT discount is a method to reduce the taxable portion of a capital gain for eligible Australian residents. By reducing the amount of profit that is actually taxed, the capital gains tax discount australia offers a significant advantage to those who practice patient stewardship of their wealth. This discount typically applies to a wide range of assets that form the backbone of many retirement plans, including shares, managed funds, and investment properties. Understanding how this discount works is the first step in ensuring your hard-earned gains are protected for your future needs.

The 12-Month Ownership Rule

To access the discount, you generally need to have owned the asset for at least 12 months. One common point of confusion is when that 12-month clock actually starts. While many people assume the settlement date is the trigger, the ATO actually looks at the date you signed the contract. This distinction is vital. If you sign a contract to sell a property even one day before your 12-month anniversary of the purchase contract, you could lose the entire discount. The ATO calculates this as a 365-day holding period, excluding the day of acquisition and the day of disposal. There are rare exceptions, such as if an asset is lost or destroyed and you receive an insurance payout, where the holding period requirements might be treated differently.

Who is Eligible for the Discount?

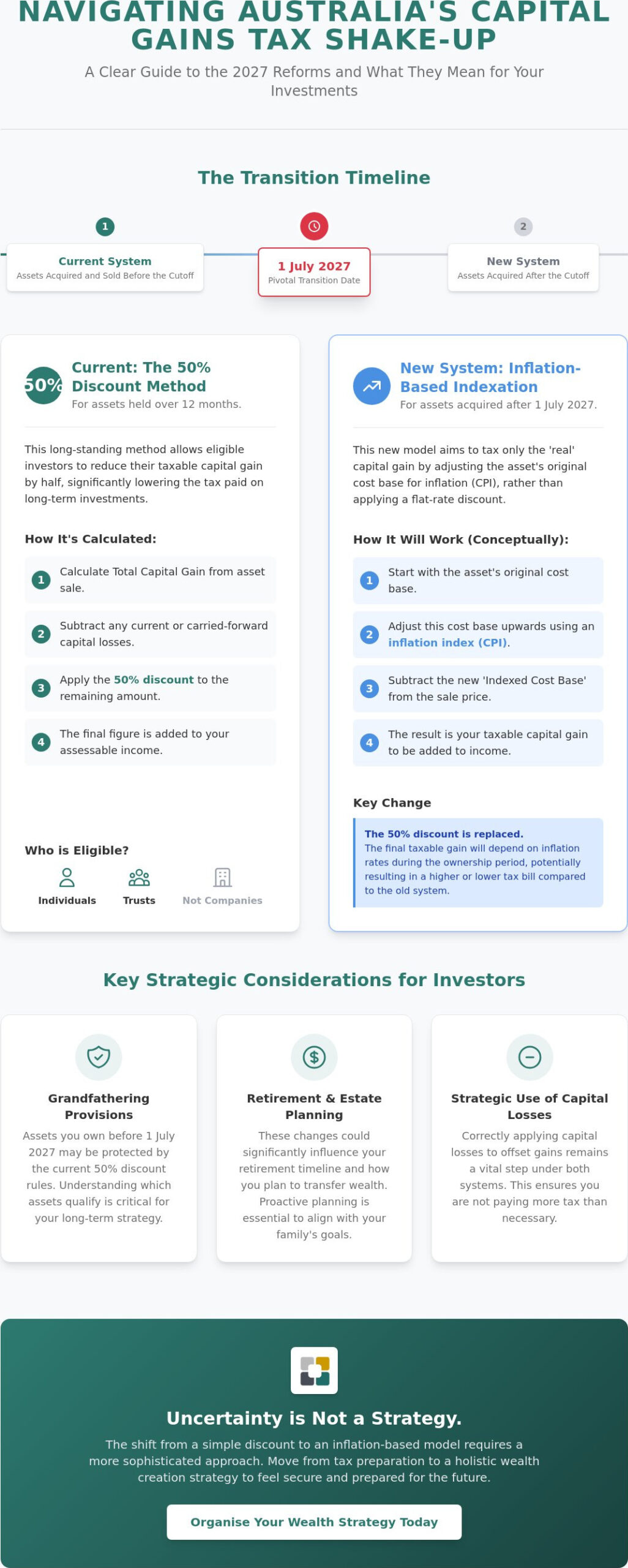

The discount is primarily designed for individuals and trusts. If you are investing in your own name or through a family trust, you can generally access the 50% reduction on your capital gains. Companies, however, are excluded from this benefit. They are taxed on the full amount of their capital gains at the corporate tax rate. As of June 2026, eligibility is also strictly tied to your residency status. Australian residents for tax purposes enjoy the full benefit, but temporary residents or foreign residents generally cannot claim the discount on gains that accrued while they were non-residents. If your circumstances involve living or working overseas, it is wise to look closely at how your residency status aligns with your investment timeline to avoid an unexpected tax bill.

Current CGT Rules: The 50% Discount Method

For over two decades, the 50% discount has been the cornerstone of investment planning for everyday Australians. It is a straightforward way to ensure you aren’t taxed on the full value of your hard-earned growth. While The 2026-27 Budget Reforms signal a shift in the wind, understanding the current capital gains tax discount australia rules remains essential for managing your assets today. This method provides a sense of certainty, allowing you to estimate your future tax obligations with relative ease as you work toward your retirement goals.

The process involves more than just halving your profit. First, you must identify your total capital gains for the financial year. Before applying any discount, you are required to subtract any capital losses you’ve incurred during the same period. If you have “carried-forward” losses from previous years, these must also be deducted. Only after these offsets are applied can you reduce the remaining amount by 50%. This final figure is your net capital gain, which is then added to your other income. Because this gain is taxed at your marginal rate, your overall income for the year will ultimately determine how much tax you pay on that profit.

Calculating Your Net Capital Gain

It’s a common misconception that you can apply the discount to a loss to reduce your tax bill. In reality, the discount only applies to the profit that remains after all losses are accounted for. This means if you have a $20,000 gain and a $5,000 loss, you apply the 50% discount to the remaining $15,000. If your losses outweigh your gains, you cannot use the capital gains tax discount australia to create a bigger tax deduction. Instead, that net loss is carried forward to future years. Staying on top of these calculations is a vital part of professional tax return preparation, ensuring you never pay more than is legally required.

Record Keeping for Future Peace of Mind

Stewardship of your wealth requires a clear paper trail. You should keep purchase and sale contracts, receipts for stamp duty, and records of any capital improvements like a home renovation or share brokerage fees. These documents form the “cost base” of your asset. Under Australian law, you must generally keep these records for five years after the asset is sold. The good news for the modern investor is that the ATO accepts clear digital copies. Transitioning to a digital filing system can reduce clutter while ensuring you are prepared for any future audits or queries. Being organised now saves significant stress when it eventually comes time to sell.

The 2026-27 Budget Reforms: Moving to an Inflation-Based Discount

The landscape of the capital gains tax discount australia has relied upon for decades is undergoing a fundamental shift. On 1 July 2027, the flat 50% discount will begin its sunset phase, replaced by a model that revives the concept of “real” gains. This means the tax office will now account for inflation when calculating your profit. If your asset’s value rises simply because the cost of living has gone up, that portion of the growth won’t be taxed. The government’s stated aim is to move capital toward more productive investments, such as new housing supply and small business growth, rather than simply rewarding the long-term holding of existing assets. It’s a change in philosophy that requires a fresh look at how we grow our wealth.

For many of our clients, the most striking part of the reform is the introduction of a minimum 30% tax on substantial net capital gains. This floor is designed to ensure that even after indexation is applied, significant wealth growth contributes a baseline amount to the national budget. If you are managing a high-value portfolio or a discretionary trust, this change could significantly alter your net returns. Understanding these nuances is the key to maintaining your peace of mind as the rules of the game evolve.

Comparing the Old vs. New CGT Regimes

To see how this affects your pocket, let’s look at a hypothetical $100,000 gain on an investment held for several years. Under the old system, you simply halved the gain and paid tax on $50,000 at your marginal rate. Under the new rules, if inflation accounted for $20,000 of that growth, you would be taxed on the remaining $80,000. If the 30% minimum tax applies, you would face a tax bill of at least $24,000, regardless of your other income levels. This move ensures that the “real” profit is what matters most to the tax office.

| Feature | Current System (Pre-July 2027) | New Reform System (Post-July 2027) |

|---|---|---|

| Primary Benefit | 50% Flat Discount | Inflation-Based Indexation |

| Tax Floor | No minimum (Marginal rate) | 30% Minimum Tax on net gains |

| Pre-1985 Assets | Generally Exempt | Taxable (Apportioned from 2027) |

What the Transition Means for Your 2026 Strategy

Does this mean you should rush to sell your assets? Not necessarily. The transition includes specific provisions where gains are apportioned. Growth accrued up to 30 June 2027 will still be eligible for the 50% capital gains tax discount australia currently offers, while growth after that date falls under the indexation rules. This makes 2026 a critical “bridge year” for your financial strategy. Even assets acquired before September 1985, which were once entirely exempt, will be brought into the regime. It’s a vital time to sit down with a guide to determine if a “trigger event,” such as a planned sale or portfolio rebalance, should be brought forward to protect your hard-earned nest egg.

Strategic Implications for Retirement and Estate Planning

Retirement planning is often viewed through the lens of accumulation, but the “exit strategy” is where the real complexity lies. If you’ve been counting on the 50% capital gains tax discount australia currently provides to fund your post-work years, the 2027 shift might feel like a hurdle. It’s important to remember that tax is simply one variable in your broader journey. By taking a proactive approach to stewardship now, you can ensure that your retirement timeline remains intact. Have you considered how a change in your expected tax bill might affect your travel plans or your ability to support your grandchildren?

Superannuation continues to be one of the most effective ways to manage tax. Because assets within the pension phase often enjoy significant tax exemptions, moving wealth into this environment before the 2027 reforms take hold could be a wise move. It’s about finding the balance between your current needs and your future peace of mind. This isn’t just about spreadsheets; it’s about the security of knowing your home and your lifestyle are protected. When we look at your wealth as a tool for your life goals, the tax changes become a puzzle to solve rather than a barrier to your success.

CGT and Your Retirement Income

If you are planning to sell an investment property to fund your lifestyle, the timing of that sale is now more critical than ever. Under the new rules, the inflation-indexed gain might result in a higher tax bill than the old flat discount, especially if the property has seen massive growth far above the inflation rate. One strategy to consider is staggering the disposal of assets over several financial years. This if-then logic allows you to potentially stay within lower marginal tax brackets and preserve more of your nest egg. For those with properties acquired after 12 May 2026, the limits on negative gearing for existing builds further emphasise the need for a clear, integrated cash flow plan that looks at the whole picture.

Estate Planning: Passing on Assets

When it comes to your family’s future, the rules around inherited assets can be particularly confusing. Currently, beneficiaries often inherit the cost base of the deceased, but the 2027 reforms will introduce new layers to how these gains are calculated. Will your children be able to claim the 50% capital gains tax discount australia offers today on growth that happened decades ago? Professional estate planning advice is essential here to ensure your legacy isn’t eroded by avoidable tax liabilities. We can help you organise your affairs so that your heirs receive the full benefit of your lifelong hard work. Taking these steps now is a gift of clarity to your loved ones, reducing the administrative burden during an already difficult time.

How Financial Mentors Can Guide Your Tax Strategy

Navigating the transition from the familiar 50% capital gains tax discount australia has relied on for decades requires more than just a calculator. It requires a partner who understands that these numbers represent your life’s work and your family’s future. While the 2026-27 budget changes might feel like a source of uncertainty, we see them as an opportunity to refine your financial roadmap. Our role as your trusted guide is to help you look past the immediate confusion of the 1 July 2027 cutoff and focus on the steady progress of your long-term goals. We believe that when you have a clear understanding of your position, the anxiety of change is replaced by the confidence of being prepared.

A wise mentor doesn’t just look at a single tax year; they look at the whole picture of your life. We consider how your tax obligations intersect with your retirement aspirations and your estate planning goals. If we identify that your current asset structure could lead to a higher tax bill under the new inflation-based rules, we can work together to explore rebalancing your portfolio before the transition date. This holistic approach ensures that your wealth creation strategies are not just compliant with the law, but are actively working to protect your hard-earned nest egg.

Integrated Tax and Wealth Services

If you’ve ever felt that your tax preparer and your financial planner were speaking different languages, you’re not alone. We believe that true stewardship comes from alignment. By having your tax return preparation handled by the same office that manages your wealth, you ensure that every deduction and every capital gain is viewed through a strategic lens. This integration allows us to identify opportunities for tax-effective wealth creation well before the 2027 deadline. Our commitment is to provide plain English advice that avoids industry jargon, empowering you to make wise decisions about your future with absolute clarity.

Taking the Next Step Toward Security

We encourage you to organise a comprehensive review of your investment portfolio today to ensure you are positioned correctly for the upcoming reforms. There is a deep sense of peace that comes from having a documented financial roadmap that accounts for the sunsetting of the current capital gains tax discount australia rules. This roadmap isn’t just a set of numbers; it’s a promise to yourself and your family that your future is secure. If you’re ready to move beyond simple tax compliance and toward a partnership focused on your long-term well-being, we invite you to start a conversation with us. Let’s look at your unique aspirations and build a plan that carries you through the 2026-27 reforms and beyond.

Preparing Your Portfolio for the Road Ahead

The shift from a flat 50% discount to an inflation-indexed system marks a significant turning point for many Australian investors. By understanding the 1 July 2027 transition and how it affects your specific assets, you can turn a period of uncertainty into a strategic advantage. Whether you’re considering the timing of a property sale or looking to protect an inheritance for your children, the right preparation ensures your wealth continues to serve your personal aspirations. Professional stewardship is about more than just numbers; it’s about the security of knowing your plans are on firm ground.

Our team has been supporting Australians with AFSL licensed advice since 2003, specialising in the complex intersections of retirement and estate planning. We provide a unique, integrated approach that combines tax return preparation with holistic wealth management. This ensures that every decision regarding the capital gains tax discount australia offers today is perfectly aligned with your long-term security and peace of mind.

Secure your future—speak with a Financial Mentor about your CGT strategy today.

You don’t have to navigate these legislative changes alone. We are here to walk beside you, providing the steady guidance you need to reach your milestones with confidence.

Frequently Asked Questions

Is the 50% CGT discount being abolished in Australia?

The 50% discount is being phased out for gains realised from 1 July 2027 onwards. Under the Treasury Laws Amendment (Tax Reform No. 1) Bill 2026, it will be replaced by a system based on inflation indexation. This means if you sell an asset after the cutoff, you will only pay tax on growth that exceeds the inflation rate. It’s a significant shift from the flat 50% reduction we’ve used for years.

How does the 12-month rule work for the CGT discount in 2026?

To qualify for the discount in 2026, you must hold your asset for at least 365 days. The ATO measures this from the date you sign the purchase contract to the date you sign the sale contract, not the settlement dates. If you sell even one day early, you lose the entire benefit. We recommend checking your original contracts to ensure your timing is exact and your wealth is protected.

What is the “minimum 30% tax” on capital gains announced in the budget?

The minimum 30% tax is a new floor rate for substantial net capital gains realised after 1 July 2027. This change ensures that high-value gains contribute a baseline amount to the budget, regardless of other offsets. If your net gain is significant, you may face this 30% rate even if your marginal tax rate is lower. It’s a move designed to target high-net-worth wealth creation strategies more directly.

Can I still use the 50% discount if I sell my property before 1 July 2027?

Yes, you can still access the 50% capital gains tax discount australia currently offers if you finalise your sale before 1 July 2027. This makes the 2026-27 financial year a critical window for those considering selling long-held assets. If your contract is signed before the transition date, your gain will be calculated under the existing rules. This provides a clear opportunity to lock in the 50% reduction before the new system begins.

How do capital losses affect my CGT discount eligibility?

You must apply your capital losses against your capital gains before any discount is calculated. If you have losses from the current year or carried forward from the past, these reduce your total gain first. The 50% discount then applies only to the remaining net amount. It’s a common area of confusion, but getting this order right is vital for accurate tax return preparation and avoiding ATO queries.

Does the CGT discount apply to my primary place of residence?

Your primary place of residence is generally exempt from CGT altogether under the main residence exemption. This means you don’t need a discount because you aren’t paying tax on the growth of your home. However, if you’ve used part of your home for business or rented it out, you might only get a partial exemption. In those cases, the capital gains tax discount australia provides would apply to the taxable portion of your gain.

What is the difference between the discount method and the indexation method?

The discount method simply halves your taxable gain, while the indexation method adjusts your asset’s cost base for inflation. From July 2027, the flat 50% reduction disappears for most investors. Instead, you’ll calculate your profit by subtracting the inflation-adjusted purchase price from your sale price. This ensures you’re only taxed on “real” growth. It’s a return to a model that was common in Australia before 1999.

Will the 2026-27 reforms affect my superannuation investments?

While the primary focus of these reforms is on individuals and trusts, your superannuation strategy may still need a review. Super funds currently benefit from a one third discount, bringing their effective CGT rate to 10% for assets held over a year. The government’s shift toward productive investment and new housing supply may influence how fund managers allocate your retirement savings. It’s a good time to ensure your super remains aligned with your goals.