Imagine standing at the threshold of your final day at work, feeling the weight of decades of effort finally lifting, only to find yourself staring at a complex web of rules rather than the clear path you expected. It’s a common moment of reflection for many Australians considering their superannuation retirement options. You’ve spent years diligently growing your savings, yet the transition to actually using that money can feel like learning a whole new language. If you’ve found yourself lying awake wondering how to navigate the $2.1 million transfer balance cap or exactly when you meet a “condition of release,” you aren’t alone in that uncertainty.

We believe you deserve to feel confident that your money is working just as hard as you did. This guide aims to simplify the process, ensuring your transition into this new stage of life is as smooth and worry-free as possible. We’ll provide a clear, jargon-free roadmap of the choices available to you, from setting up a steady income stream to protecting your family’s inheritance. You’ll discover how to manage your funds for a stable future while keeping the latest regulations in perspective, giving you the peace of mind to focus on the retirement you’ve earned.

Key Takeaways

- Learn how reaching your preservation age and meeting a condition of release transforms your super from a locked savings account into a flexible resource for your future.

- Compare various superannuation retirement options, such as taking a lump sum or establishing a steady income stream, to see which path best supports your unique lifestyle goals.

- Discover how a Transition to Retirement strategy can help you reduce your working hours without compromising your current income or your long-term savings.

- Understand how your superannuation balance interacts with Centrelink’s asset and income tests to help you maximise your eligibility for the Age Pension.

- Ensure your hard-earned savings go to the right people by learning why death benefit nominations are vital for protecting your family’s inheritance.

The Retirement Transition: What Happens to Your Super When You Finish Work?

That first Monday morning without an alarm clock is a milestone you’ve spent decades working towards. It’s a significant shift in your daily rhythm, but it also marks a profound change in your relationship with your finances. For years, you’ve been an accumulator, watching your balance grow through consistent effort and compound interest. Now, the focus turns to how you’ll use those savings to fund the life you’ve imagined. This transition requires a new mindset of stewardship. If you treat your super as a carefully managed tool for your future self, you can move from a place of uncertainty to one of quiet confidence.

With 2026 bringing updated thresholds, such as the $2.1 million transfer balance cap and new contribution limits, it’s a vital year to review your settings. You aren’t just choosing a financial product; you’re designing the next twenty or thirty years of your life. Understanding your superannuation retirement options is the first step in ensuring that “Day One” of your retirement is the beginning of a relaxed and fulfilling chapter, rather than a source of administrative stress.

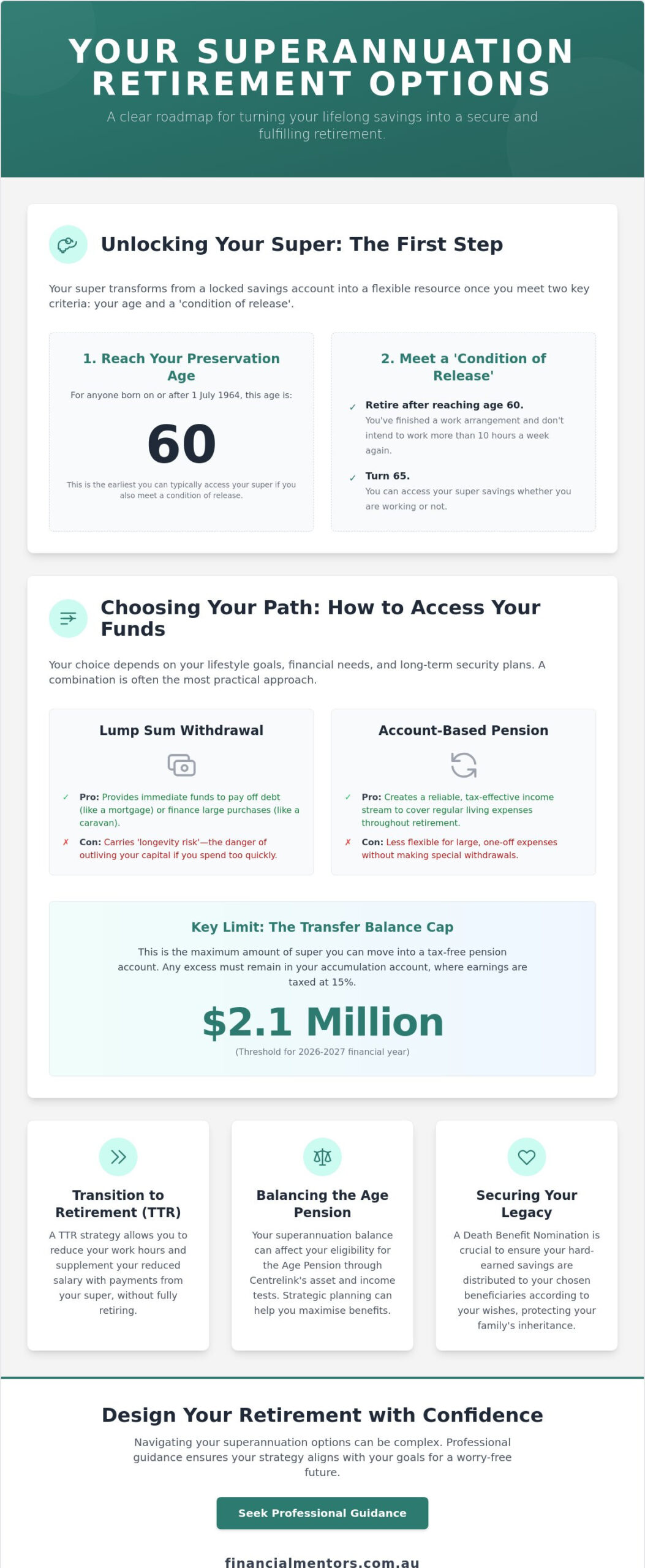

Meeting the Condition of Release

The rules governing Superannuation in Australia ensure your money is there when you need it most. If you were born on or after 1 July 1964, your preservation age is 60. Meeting a “condition of release” usually involves reaching this age and retiring. The ATO views you as retired if you finish a work arrangement after 60 or if you don’t intend to work more than 10 hours a week again. Once you turn 65, these restrictions disappear. You can then access your savings regardless of whether you’re still working or have fully retired.

Why Your ‘Day One’ Strategy Matters

Transitioning into retirement can feel overwhelming without a clear plan. Many Australians face “frozen indecision,” keeping their funds in sub-optimal accounts because the technical details seem too complex. Others might make hasty withdrawals that trigger unnecessary tax liabilities. Partnering with a guide for your retirement planning helps you set concrete goals for your first five years. Whether you’re planning a lap of the map or simply want a stable income, a structured approach to your superannuation retirement options ensures your money is ready to support you from the moment you stop working.

Have you considered how your spending might change in those early years compared to later in life? By defining your priorities now, you can create a roadmap that balances your desire for immediate adventure with the need for long-term security. This proactive planning is what transforms a simple fund into a lifelong support system.

Exploring Your Core Superannuation Retirement Options

Once you meet a condition of release, you face a significant choice about how to structure your wealth. There isn’t a one-size-fits-all answer. Your decision depends on your personal goals and your vision for the future. Understanding the different Types of super funds and account structures is essential here. Generally, your superannuation retirement options fall into three main categories: taking a lump sum, starting an account-based pension, or a thoughtful combination of both.

A combination approach is often the most practical path for modern retirees. You might take a small lump sum to handle immediate needs and move the rest into a pension. This gives you the “best of both worlds” by providing flexibility and a steady income. As you plan this transition, keep the Transfer Balance Cap in mind. For the 2026-2027 financial year, this cap is $2.1 million. This is the maximum amount of super you can move into a tax-free pension account. If your balance exceeds this, the excess stays in your accumulation account where earnings are taxed at 15%.

The Pros and Cons of Lump Sum Withdrawals

Taking a lump sum can be incredibly liberating. It’s often the quickest way to clear a remaining mortgage or fund a long-held dream, like a caravan trip around the coast. However, it’s a decision that requires careful thought. If you’re under 60, there may be tax implications to consider. More importantly, there’s the “longevity risk.” This is the very real possibility of outliving your capital if you spend too much too early. It’s about balancing today’s freedom with tomorrow’s security.

Understanding Account-Based Pensions

For many, an account-based pension offers the most peace of mind. It mimics the regular paycheque you’ve relied on for years. This makes budgeting much simpler. If you’re over 60, the investment earnings within this pension phase are typically tax-free. This is a powerful benefit that helps your money work harder. You do need to be aware of minimum withdrawal requirements. The government expects you to take a certain percentage of your balance each year, which increases as you get older. These superannuation retirement options are designed to ensure your savings last throughout your lifetime.

Managing these thresholds while aiming for a worry-free lifestyle can feel like a balancing act. If you’re feeling unsure about which path fits your life best, seeking professional retirement planning can provide the clarity you need to move forward with confidence.

Transition to Retirement (TTR) vs. Full Retirement

Retirement doesn’t have to be a sudden stop. For many Australians, the idea of walking away from a career on a Friday and doing nothing on a Monday is quite daunting. This is where a Transition to Retirement strategy becomes one of the most valuable superannuation retirement options. It acts as a bridge, allowing you to wind back your working hours while using your super to maintain your current lifestyle. Instead of a “cliff,” you get a ramp that lets you ease into your new chapter with confidence and financial stability.

One of the most effective ways to use this period is through a strategy often called “income recycling.” If you’re still working full-time or even four days a week, you might choose to salary sacrifice a larger portion of your income into your super. To make up for the lower take-home pay, you then draw a pension from your TTR account. Because you’re over 60, the pension payments you receive are generally tax-free, while the contributions going into your super are taxed at the lower concessional rate of 15%. This clever bit of organising can help you boost your final balance significantly in those last few years of work.

The TTR Strategy for Over 60s

If you’ve reached your preservation age of 60 but aren’t ready for a full stop, a TTR pension can supplement a part-time salary beautifully. It allows you to say “yes” to three-day weeks without worrying about how you’ll pay the bills. You get to keep your skills sharp and stay socially connected while reclaiming your time for hobbies or family. It’s vital to remember that TTR earnings remain taxed at 15% until full retirement. This is a key difference compared to a full retirement pension, where investment earnings inside the fund are typically tax-free.

When to Make the Full Switch

Identifying the tipping point where full retirement makes financial sense is a deeply personal process. For some, it’s when they reach the $2.1 million transfer balance cap; for others, it’s simply when the pull of the golf course or the garden becomes too strong to ignore. Moving from a TTR to a full retirement pension involves an administrative shift where you notify your fund that you’ve met a final condition of release. This simple step unlocks the tax-free status on your fund’s investment earnings. Seeking professional retirement planning ensures the timing of this switch aligns perfectly with your broader tax goals and lifestyle aspirations. We can help you navigate these superannuation retirement options so you can focus on the joy of your newfound freedom.

Balancing Your Super with the Age Pension and Other Income

A comfortable retirement often feels like a puzzle where all the pieces must fit together perfectly. While your super is a primary pillar, the Age Pension remains a vital safety net for about seven out of ten Australian retirees, according to data from March 2026. Finding the right balance between your private savings and government support is a key part of exploring your superannuation retirement options. It’s about making sure every dollar you’ve saved works in harmony with the benefits you’ve earned through years of contributing to the community.

This coordination is especially important when you consider your non-super assets. If you own your home, you already have a significant advantage, as your principal place of residence is typically exempt from Centrelink’s tests. However, other investments like holiday homes, shares, or even the value of your cars will be part of the calculation. By looking at your wealth as a single, organised strategy, you can avoid the stress of unexpected changes to your pension payments.

Navigating the Asset and Income Tests

Centrelink uses two distinct tests to determine your eligibility, and they’ll apply the one that results in the lower pension rate. Most of your financial assets are subject to “deeming rules.” These rules assume your investments earn a set rate of return, regardless of what they actually pay. As of March 2026, the lower deeming rate is 1.25%, while the upper rate is 3.25% for assets above the threshold. It’s a methodical system, but it can feel complex. Keeping Centrelink informed about your changing circumstances, such as a major home renovation or a gift to family, is essential to ensure your records remain accurate.

Maximising Your Total Retirement Income

There is often a “sweet spot” where your super withdrawals and a part-pension meet to provide a very stable lifestyle. Even if your assets currently sit just above the limit for a pension, you might still be eligible for the Commonwealth Seniors Health Card. This card provides significant relief through cheaper medicines and discounts on various utilities. If you want to ensure your strategy is truly future-proofed, our team can provide expert retirement planning to help you optimise your eligibility and bridge the gap between your savings and government support. We can help you navigate these superannuation retirement options so you can focus on enjoying the time you’ve worked so hard to reach.

Organising Your Legacy: Why Professional Guidance Makes the Difference

While you’ve spent years deciding which superannuation retirement options will best fund your own lifestyle, the final step in your journey is ensuring that any remaining wealth is passed on exactly as you intended. It’s a common surprise for many Australians to learn that their superannuation is not automatically covered by their Will. Because super is held in a trust, it sits outside your personal estate. This means that even with a perfectly drafted legal document, your hard-earned savings could be distributed in a way you didn’t expect if your fund’s records aren’t up to date.

Thinking about your legacy is an act of stewardship for the people you love. By coordinating your retirement strategy with your estate planning goals, you ensure that your money continues to provide security for your family long after you’ve finished using it. This is where the role of a wise mentor becomes invaluable. We help you look at the big picture, ensuring that the technical settings of your fund align with your heart’s desires for your children and grandchildren.

Protecting Your Beneficiaries

To give your family certitude, you need to consider the type of death benefit nomination you have in place. A binding nomination provides the most certainty, as it legally requires the fund to pay your balance to your chosen beneficiaries. In contrast, a non-binding nomination only acts as a guide, leaving the final decision to the fund’s trustee. You also need to be mindful of the “Death Tax.” If your super is paid as a lump sum to an adult child who is no longer financially dependant on you, the taxable component is generally subject to a 15% tax plus the Medicare levy. A reversionary pension is a practical way to support a spouse, as it allows your income stream to continue automatically to them after you pass away without the funds leaving the tax-effective super environment.

The Financial Mentors Approach to Your Future

At Financial Mentors Wealth Management, we believe your retirement should be defined by peace of mind rather than paperwork. We move beyond simple compliance to focus on true wealth protection and the realisation of your personal goals. With new legislation introducing an additional 15% tax on earnings for super balances over $3 million from 1 July 2026, the way you structure your superannuation retirement options and legacy has never been more important. Our tailored financial roadmaps are designed to reduce the stress of these complex decisions, giving you a clear path forward.

If you’re ready to secure your legacy and gain clarity on the years ahead, we’re here to help. Book a consultation with Financial Mentors to organise your retirement and ensure your hard work benefits your family for generations to come.

Your Path to a Confident Retirement

Choosing between various superannuation retirement options doesn’t have to be a source of anxiety. By understanding how to balance regular income streams with the flexibility of lump sums, you can create a lifestyle that truly reflects your values. Whether you are navigating the 2026 transfer balance caps or organising your legacy to protect your family’s inheritance, the most important step is having a clear, personalised roadmap. It’s about ensuring your hard work translates into the worry-free future you’ve earned.

At Financial Mentors, we’ve been providing specialist expertise in retirement and estate planning since 2003. As an AFSL registered firm, we pride ourselves on a human-centric, empathetic advice model that puts your peace of mind first. We don’t just see numbers; we see the aspirations you’ve held for years. If you’re ready to move forward with a plan that feels right for you, start your retirement journey with a trusted mentor at Financial Mentors. We’re here to help you step into this next chapter with quiet confidence and the stability you deserve.

Frequently Asked Questions

Can I withdraw all my super as a lump sum when I turn 60?

You can generally withdraw your super as a lump sum once you turn 60 and meet a condition of release, such as retiring. If you reach age 60 and finish a work arrangement, the ATO typically considers you retired, granting you full access to your savings. If you continue working, you can still access your funds after you turn 65 regardless of your employment status. It’s a significant decision that affects your long-term capital, so careful planning is essential.

What is the difference between a transition to retirement pension and a normal pension?

The primary difference is your work status and the tax treatment of the investment earnings within your fund. A transition to retirement (TTR) pension is designed for those still in the workforce who want to supplement their income, and the fund’s earnings are taxed at 15%. A normal account-based pension is for those who have fully retired or turned 65. In this retirement phase, the investment earnings inside the fund are typically tax-free, making it a highly efficient way to manage your wealth.

How much super do I need to have a comfortable retirement in Australia?

There isn’t a single figure that fits every Australian, as the amount depends on your personal lifestyle goals and whether you own your home. The retirement system is designed for super and the Age Pension to work together, with the pension supporting about seven out of ten retirees as of 2026. Rather than focusing on a generic industry number, we help you determine a balance that ensures your money supports your specific aspirations while providing long-term security.

Will my super balance stop me from getting the Age Pension?

Your super balance is included in Centrelink’s asset and income tests, which can reduce your pension payments or affect your eligibility. If your assets exceed the thresholds set by the government, your pension rate will decrease. However, many people find a “sweet spot” where their superannuation retirement options and a part-pension combine to provide a stable income. Even if you don’t qualify for the pension, you might still be eligible for the Commonwealth Seniors Health Card and its associated benefits.

What happens to my super if I die before I use it all?

Your remaining superannuation is distributed to your beneficiaries or your estate based on the death benefit nominations you have made with your fund. Because super isn’t automatically part of your Will, having a binding nomination is the most certain way to ensure your wishes are followed. If the balance is paid to a non-tax dependant, such as an independent adult child, there may be tax implications. Organising these details now ensures your family is protected and your legacy is preserved.

Is it better to take a lump sum or a pension for tax purposes?

For most people over 60, both lump sums and pension payments are tax-free, but the pension phase offers superior tax efficiency for your remaining balance. When you move your money into an account-based pension, the investment earnings generated within that account are generally tax-free. If you take a large lump sum and invest it elsewhere, you may be liable for tax on any interest or dividends earned. Evaluating these superannuation retirement options helps you keep more of your hard-earned money working for you.

Can I still contribute to my super once I have started a pension?

You can still make contributions to a separate accumulation account even after you have commenced a pension, provided you are under age 75. For the 2026-2027 financial year, the concessional contribution cap is $32,500 and the non-concessional cap is $130,000. You cannot add fresh capital directly into an existing pension account. Instead, you would keep those new contributions in an accumulation account or eventually start a second pension if that suits your broader financial strategy.

How often can I change my superannuation retirement options?

You can generally review and adjust your retirement settings at any time, although some changes may involve administrative steps or tax considerations. Retirement is a long-term transition, and it’s natural for your needs to evolve as you move through different stages of life. We view your financial plan as a living document that should be refined as your circumstances change. Regular reviews ensure your strategy remains aligned with your goals, providing the peace of mind that comes from being well-prepared.