If you’ve spent decades dedicated to the Australian public service, is your reward a secure future or a mountain of paperwork you’re afraid to sign? It’s a common feeling for those approaching the end of a long career. The very benefits designed to look after you, like the PSS or CSS, often feel like a puzzle with missing pieces. You deserve to feel confident about the path ahead rather than worried about making a choice you can’t undo. Proper public sector retirement planning australia is about more than just numbers; it’s about ensuring your hard work translates into a lifestyle that supports you and your loved ones.

In this guide, we’ll help you find a clear way forward by exploring how to maximise your defined benefit options and manage the interaction with the Age Pension. You’ll discover how to structure a tax-effective transition to retirement that provides the peace of mind you’ve earned. If we can map out your legacy benefits with care today, then you can step into your next chapter with quiet confidence and a sense of true security. This roadmap is designed to simplify the complex, protecting your spouse and your estate while you focus on the life you’ve planned.

Key Takeaways

- Understand the fundamental differences between government and private sector superannuation to better appreciate the unique value of your legacy benefits.

- Gain clarity on public sector retirement planning australia by decoding the specific rules governing PSS, CSS, and modern CSC-managed funds.

- Weigh the long-term benefits of CPI-indexed pensions against lump sum options to ensure your retirement income remains stable in any economic climate.

- Learn how strategic tax return preparation and navigating the Transfer Balance Cap are essential steps for a tax-effective transition to retirement.

- Discover how partnering with a trusted guide can help you organise your estate and protect your spouse through personalised financial planning.

Navigating the Unique Landscape of Public Sector Retirement in Australia

For most Australians, retirement is a matter of checking a balance and hoping the market remained steady. If you’ve dedicated your career to the public service, your reality is quite different. Your path doesn’t just follow the general trends of Superannuation in Australia; it involves managing a complex legacy of benefits unique to government employment. This is why a generic, one-size-fits-all approach often falls short for public servants. You aren’t just saving money; you’re acting as a steward for a life’s work. It’s about protecting a promise made to you when you first stepped into your role.

The landscape of public sector retirement planning australia has changed significantly over the decades. Between the closure of legacy schemes in the early 2000s and the updated contribution caps set for the 2026-27 financial year, the rules have shifted. If you joined the service before 2005, you likely have access to benefits that your private-sector peers simply cannot replicate. Understanding these differences is the first step toward a secure future. It requires a patient, thoughtful look at how your specific fund works within the broader Australian system.

The Shift from Defined Benefit to Accumulation Schemes

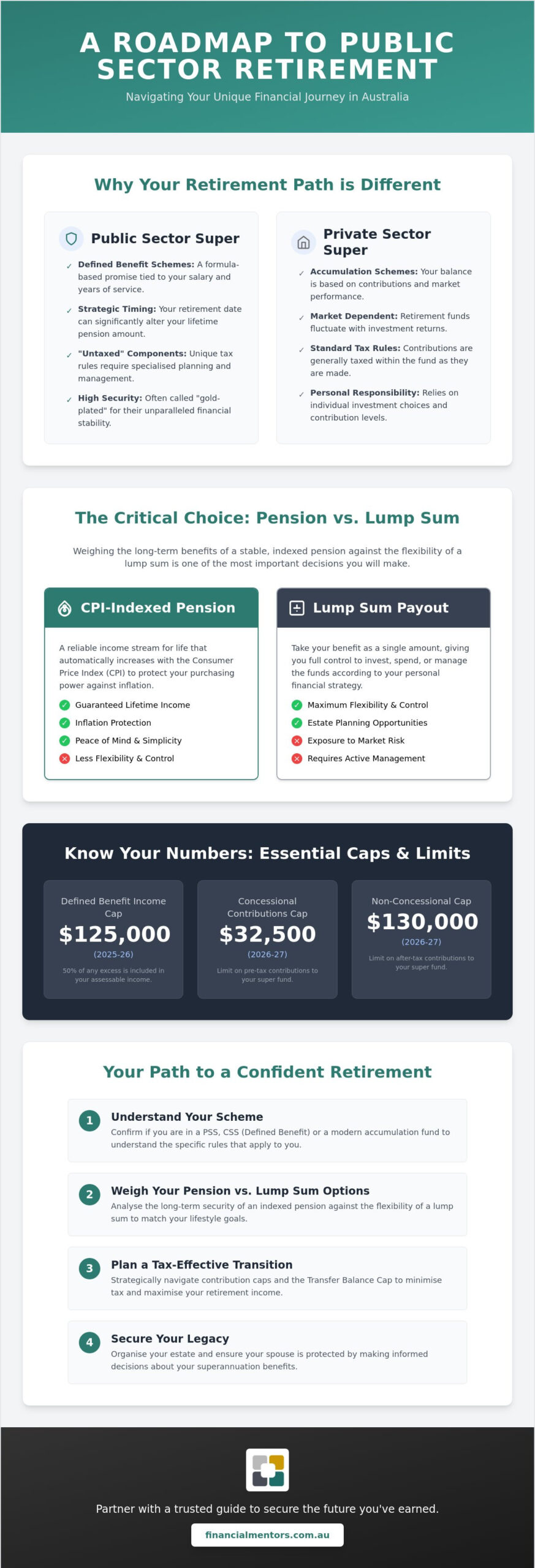

Historically, government super was built on a promise rather than just a pot of money. A Defined Benefit Scheme is a formula-based retirement promise, usually tied to how long you served and what you earned. While newer employees who joined after 2005 are typically in accumulation funds like the PSSap, many long-term staff remain in the PSS or CSS. Knowing which category you fit into changes everything about how you plan. If you’re in a legacy scheme, your focus is on maximising a formula; if you’re in an accumulation fund, your focus is on market growth and contributions.

Why Timing Your Exit Matters More in the Public Service

In the public sector, your retirement date isn’t just a day on the calendar. It’s a strategic lever. Because benefits are often calculated using your final average salary and total years of service, retiring a few months earlier or later can make a noticeable difference to your lifetime indexed pension. It’s a high-stakes decision that deserves careful calculation.

The transition is emotional too. Moving from the stability of a government department to a self-funded life requires a mental shift. Ask yourself: am I retiring from a job I’m tired of, or to a life I’ve carefully built? If you can answer that with clarity, the financial decisions become much easier to manage. Taking the time to reflect on your personal goals ensures that your retirement roadmap leads exactly where you want to go.

Decoding Legacy Schemes: PSS, CSS, and Modern Alternatives

The Commonwealth Superannuation Corporation (CSC) manages the financial backbone of many government careers. If you’ve been in the service for a long time, your fund likely contains “untaxed” components. This is a unique feature where tax hasn’t been paid on the employer’s contributions yet. It’s quite different from the private sector, and it means your strategy needs to be precise. For the 2026-27 financial year, the concessional contribution cap is $32,500, while the non-concessional cap is $130,000. Managing these limits while holding a high-value benefit requires a steady hand. While federal employees focus on CSC, those in state roles navigate schemes like GESB in WA or QSuper in QLD, which carry their own distinct rules and opportunities.

Effective public sector retirement planning australia involves understanding how these legacy benefits interact with modern tax laws. For example, if you hold a taxed defined benefit pension like the PSS, you must be mindful of the $125,000 Defined Benefit Income Cap for the 2025-26 period. If your pension exceeds this, 50% of the excess is included in your assessable income. These rules can feel like a maze, but they are also the key to unlocking a very comfortable future. If you take the time to organise your finances with a mentor who understands these nuances, the path becomes much clearer.

The PSS and CSS: Understanding Your “Defined” Future

The PSS and CSS are often called “gold-plated” because they offer levels of security rarely seen today. If you’re in the PSS, your contribution rate and the 10-year rule are vital factors in your final calculation. The CSS is even more intricate; it’s a three-part structure involving your personal contributions, the employer’s component, and a productivity top-up. Because these are defined benefit schemes, they are indexed to protect your purchasing power. In July 2026, PSS and CSS pensions will increase by 2.0% based on recent CPI movements. This guaranteed growth is a powerful tool for long-term stability.

PSSap and Modern Accumulation Funds

For those who joined after 2005, the PSSap is the standard. It operates like a private accumulation fund where your final balance depends on market performance and contribution levels. You have the flexibility to choose your investment mix or even move to a different fund if it aligns better with your personal goals. It’s also wise to evaluate the insurance benefits bundled with these accounts. Often, the death and disability cover provided within public sector funds is more comprehensive and cost-effective than what you might find in the general market.

The Transition: Choosing Between Lump Sums and Indexed Pensions

Deciding how to receive your hard-earned benefits is perhaps the most significant crossroad in public sector retirement planning australia. It’s the moment where years of service transform into a tangible future. You’re faced with a fundamental question: do you prefer the absolute certainty of a guaranteed income, or the flexibility and control of a lump sum? There isn’t a right answer for everyone, but there is a right answer for you. If we look closely at your lifestyle goals and family needs, the choice often becomes much clearer.

One of the most remarkable features of public sector pensions is their resilience. In an environment where the cost of living feels unpredictable, having a CPI-indexed income provides a rare sense of peace. For instance, PSS and CSS pensions are set to increase by 2.0% in July 2026. This adjustment ensures your purchasing power doesn’t erode over time, allowing you to maintain your standard of living regardless of what’s happening in the broader economy. It’s a “pay cheque for life” that removes the stress of market volatility from your daily thoughts.

Pros and Cons of the Lifetime Indexed Pension

The security of a lifetime pension is hard to beat, especially when you consider your loved ones. These schemes often include a “reversionary” component, meaning if you pass away, a significant portion of the pension continues for your spouse. It’s a final act of stewardship for your partner’s future. However, the trade-off is a lack of capital flexibility. You generally cannot withdraw a large amount for a sudden expense, nor can you leave the underlying capital to your children as an inheritance. You’re trading legacy for longevity.

Evaluating the Lump Sum Strategy

Choosing a lump sum puts the steering wheel firmly in your hands. If you have a mortgage to clear or dreams of a more aggressive wealth creation strategy, this path might appeal to you. It allows you to build a diversified portfolio that you can draw from as you please. A lump sum in 2026 requires a robust investment strategy to outpace inflation. Without the automatic safety net of indexation, your capital must work harder to keep up with rising costs. This path also makes your tax return preparation more involved, as you’ll be managing private investment income and capital gains rather than a straightforward government pension. If you value autonomy and have a clear plan for your estate, the lump sum offers possibilities that a pension simply cannot.

Strategic Wealth Management and Tax Compliance for Public Servants

In the lead-up to retirement, many see tax return preparation as a simple compliance task. However, for those engaged in public sector retirement planning australia, it’s actually a vital pillar of your wealth management strategy. When you transition into the pension phase, you must navigate the general Transfer Balance Cap, which is set at $2.1 million for the 2026-27 financial year. This cap limits how much super can be moved into a tax-free retirement account. If your balance exceeds this, the tax implications can be significant, making a proactive approach essential for your long-term peace of mind.

Protecting your legacy also means looking ahead to how your beneficiaries will be treated. You might have heard of the “death tax” on super. This isn’t a formal tax name, but it refers to the tax your adult children may have to pay on the taxable components of your superannuation if they aren’t financial dependants. By using specific strategies, such as a recontribution plan, you can potentially reduce this burden for your loved ones. It’s about being a wise steward of your resources, ensuring that the benefits of your hard work stay within your family. If you’re ready to secure your legacy, our team can provide the professional tax return preparation and estate planning advice you need to move forward with confidence.

Optimising Your Tax Position in Retirement

Success in retirement is often about what you keep, not just what you receive. Structuring your withdrawals to remain below key tax thresholds can save you thousands over the long run. If your scheme allows, you might even consider “catch-up” concessional contributions to boost your balance while lowering your taxable income in your final years of service. Accurate reporting is non-negotiable; even small errors in your tax return can lead to ATO penalties that chip away at your super income. A methodical approach here ensures that your transition to retirement is as tax-effective as possible.

Estate Planning: Beyond the Will

It’s a common misconception that your Will automatically covers your public sector death benefits. In reality, funds managed by the CSC often follow their own set of rules. This is where binding vs. non-binding nominations become critical. A non-binding nomination acts as a guide for the fund trustees, while a binding one gives you more control over who receives your benefit. Without a clear financial roadmap that includes specific estate planning advice, your legacy might not be distributed exactly as you intended. Taking the time to organise these details now provides the ultimate gift to your family: clarity and security during a difficult time.

Partnering with a Wise Mentor to Secure Your Financial Future

Deciding how to move forward with your benefits is a major life milestone. While the rules of public sector retirement planning australia can feel overwhelming, you don’t have to navigate them alone. If you’ve spent your career serving the community, it’s only right that you have a partner who understands the intricacies of your specific scheme. Financial Mentors Wealth Management acts as a trusted guide through the PSS and CSS maze, helping you see the possibilities that others might overlook. We don’t just look at the numbers; we look at the life you want to lead and the people you want to protect.

A personalised financial roadmap is essential because your service history is as unique as your fingerprint. Whether you’re managing an untaxed component or trying to stay within the $2.1 million Transfer Balance Cap, having integrated tax and retirement advice provides a level of clarity that generic services simply can’t offer. If we can align your wealth creation strategies with your estate planning needs, then you can step into retirement with quiet confidence. This collaboration is about steady progress and future-proofing your lifestyle so that you can enjoy the fruits of your labour without constant worry.

What to Expect from a Strategic Financial Consultation

Our process is designed to move you from a state of confusion to one of complete clarity. During a consultation, we take the time to validate your goals and reflect on your personal circumstances. We then organise your assets for maximum efficiency, ensuring your superannuation works in harmony with your other investments. This isn’t a one-off event. Retirement planning is a journey that evolves as your life changes. We remain by your side as a constant companion, adjusting your strategy to meet new challenges or opportunities as they arise.

Taking the First Step Toward Your Planned Retirement

Are you truly prepared for the “what ifs” that life might throw your way? Reflecting on your readiness today can prevent irreversible mistakes tomorrow. It’s often wise to start this conversation early, ideally between five and ten years before you plan to finish work. This window gives you the time needed to make meaningful changes to your contributions or to restructure your debt. If you’re ready to take control of your future, you can organise a consultation with Financial Mentors to review your public sector retirement strategy. Starting now ensures that when the day finally arrives, you’re stepping toward a future that is already secure.

Embrace the Certainty of a Well-Planned Retirement

Your career in the public service has been built on dedication and a commitment to the community. Now, it’s time to ensure those years of hard work translate into a future that reflects your aspirations. By understanding the intricate mechanics of your PSS or CSS benefits and navigating the tax complexities of the Transfer Balance Cap, you can secure a lifestyle that remains stable regardless of market shifts. Effective public sector retirement planning australia isn’t just about the final balance; it’s about the peace of mind that comes from knowing your spouse and estate are fully protected.

At Financial Mentors Wealth Management, we’ve acted as a trusted guide for government employees since 2003. As authorised representatives under a long-standing AFSL, we offer specialised expertise in legacy schemes combined with integrated tax return preparation and wealth management. If you’re ready to move from uncertainty to clarity, we’re here to help you organise every detail. Secure your legacy with a personalised financial roadmap from Financial Mentors Wealth Management. We look forward to partnering with you on this rewarding transition.

Common Questions About Public Sector Retirement Planning

Can I stay in the PSS or CSS if I leave the public service before retirement age?

Yes, you can certainly remain a member, but your benefit will typically become “preserved.” This means your accumulated service and contributions stay within the fund until you reach your preservation age or meet another condition of release. It’s a vital feature of public sector retirement planning australia because it allows your hard-earned benefits to remain secure while you pursue other career opportunities outside the government; for example, you might explore Traffic Control with a specialist provider like Acquired Awareness Traffic Management to see how these essential services operate.

How does the Commonwealth “untaxed” super component affect my tax return?

The untaxed component exists because tax hasn’t been paid on the employer’s contributions within the fund. When you receive this as a pension after age 60, the income is generally taxed at your marginal rate. To help balance this, you usually receive a 10% tax offset on the untaxed element, which can significantly reduce the amount of tax you owe each year.

What is the difference between a reversionary pension and a standard death benefit?

A reversionary pension is an ongoing income stream paid to an eligible spouse or dependant after your passing, typically at a rate of 67% of your original pension. In contrast, a standard death benefit is usually a one-off lump sum payment. Reversionary pensions are a highly valued feature of schemes like the PSS and CSS, offering long-term stewardship for your partner’s future.

Can I combine my public sector super with a private retail or industry fund?

You generally cannot roll a PSS or CSS defined benefit into a private retail fund while you are an active member. These schemes are unique “promises” rather than simple cash balances. However, many public servants choose to maintain a separate industry fund for additional voluntary contributions, allowing them to benefit from both a guaranteed pension and market-linked growth.

How much does a financial advisor cost when specialising in public sector schemes?

The cost of professional advice depends entirely on the complexity of your service history and the scope of the roadmap you need. Because public sector schemes involve intricate formulas and tax rules, a specialist advisor will typically provide a tailored quote after an initial consultation. This ensures the fee reflects the personalised attention your unique circumstances deserve.

Does my public sector pension reduce the amount of Age Pension I can receive?

Yes, your pension is assessed by Centrelink under both the income and assets tests. However, public sector pensions often have a “deductible amount” representing the portion of the pension that comes from your own after-tax contributions. This specific amount is not counted toward the income test, which may help you qualify for a higher portion of the Age Pension than you might expect.

What happens to my PSS/CSS if I decide to work part-time before fully retiring?

Moving to part-time work will generally affect the rate at which your benefits accrue, as your years of service are adjusted proportionally. While your “final average salary” is often still based on the full-time equivalent rate, the reduction in service hours can impact the final formula. It’s a transition that requires careful timing to ensure you don’t inadvertently reduce your lifetime pension.

Are there specific tax offsets available for Australian public sector retirees in 2026?

Retirees receiving a pension with an untaxed element are often eligible for a 10% tax offset if they are aged 60 or over. This is a key consideration for public sector retirement planning australia as it helps manage the tax liability on your annual income. Additionally, you may be eligible for the Seniors and Pensioners Tax Offset (SAPTO) depending on your total rebate income and personal circumstances.