What if your retirement wasn’t just a date on a calendar, but a carefully curated chapter of life where your only job was to enjoy the fruits of your labour? Many Australians feel a quiet weight when considering the maze of superannuation laws and the latest tax bracket shifts. It’s natural to worry about whether your savings will endure or if you are making the most of the current $30,000 concessional contribution cap. Finding the right financial planning services is about more than just numbers; it’s about finding a partner who understands that your legacy is deeply personal.

We understand that the complexity of estate planning and the fear of outliving your nest egg can be stressful. This guide will show you how to evaluate and select professional support to protect your wealth and manage your tax obligations effectively. You’ll discover how to build a clear financial roadmap that minimises liabilities and secures a dignified retirement. We will walk through the essential steps to gain confidence in your timeline, moving from uncertainty toward a future that feels both stable and bright.

Key Takeaways

- Learn why effective financial planning services are more than just investment advice, acting instead as a strategic roadmap for every major life transition.

- Understand how to verify professional credentials through the ASIC Financial Advisers Register and choose a fee model that aligns with your best interests.

- Discover the “Planned Retirement” strategy to smoothly transition from building your wealth to enjoying a steady, dignified income from your super and savings.

- See how moving beyond simple tax compliance to proactive planning can help you minimise liabilities and grow your investable surplus.

- Explore the benefits of a mentorship-based approach to wealth management, providing you with steady guidance and peace of mind for the long term.

Understanding Financial Planning Services: More Than Just Investments

Have you ever felt that managing your money feels like trying to read a map in a different language? While many people think of financial planning services as simply picking the right shares or insurance policies, the reality is much more human. It’s about creating a strategic roadmap that evolves as you do. Whether you are welcoming a new child, changing careers, or preparing for a dignified retirement, your finances should serve your life, not the other way around. This approach shifts the focus from mere wealth management to a deeper sense of life stewardship.

It’s vital to understand the difference between general product advice and tailored personal advice. General advice is often what you’ll find in a bank brochure; it doesn’t take your unique mortgage, family situation, or specific tax bracket into account. Personal advice, however, is a bespoke strategy designed specifically for your circumstances. This distinction is why the role of a Financial planner is so critical. By operating under an Australian Financial Services Licence (AFSL), these professionals are bound by strict regulations designed to protect consumers, ensuring that every recommendation is made with your best interests at heart.

The Scope of Modern Financial Advice

Modern advice covers every corner of your financial journey. For those still in the workforce, it involves building wealth creation strategies that work as hard as you do. As you approach the end of your career, the focus naturally shifts to superannuation optimisation and managing retirement income streams to ensure your lifestyle remains comfortable. It also includes essential estate planning advice. This ensures that your family’s legacy is protected and your assets reach the people you love most, providing you with peace of mind that your hard work will benefit future generations.

Why “DIY” Finances Can Be Costly

Attempting to manage complex finances alone can lead to expensive oversights that are difficult to correct later. For example, without professional guidance, you might inadvertently miss out on Centrelink or Age Pension entitlements due to misunderstood asset tests or deeming rates. Similarly, self-managed super funds (SMSF) carry heavy compliance burdens. A small administrative mistake can lead to significant penalties from the ATO. Perhaps most importantly, an expert provides a calm, objective perspective during volatile market cycles. This helps you avoid the emotional decisions that often lead to selling at the wrong time and jeopardising your long-term stability.

How to Evaluate Financial Planning Services in Australia

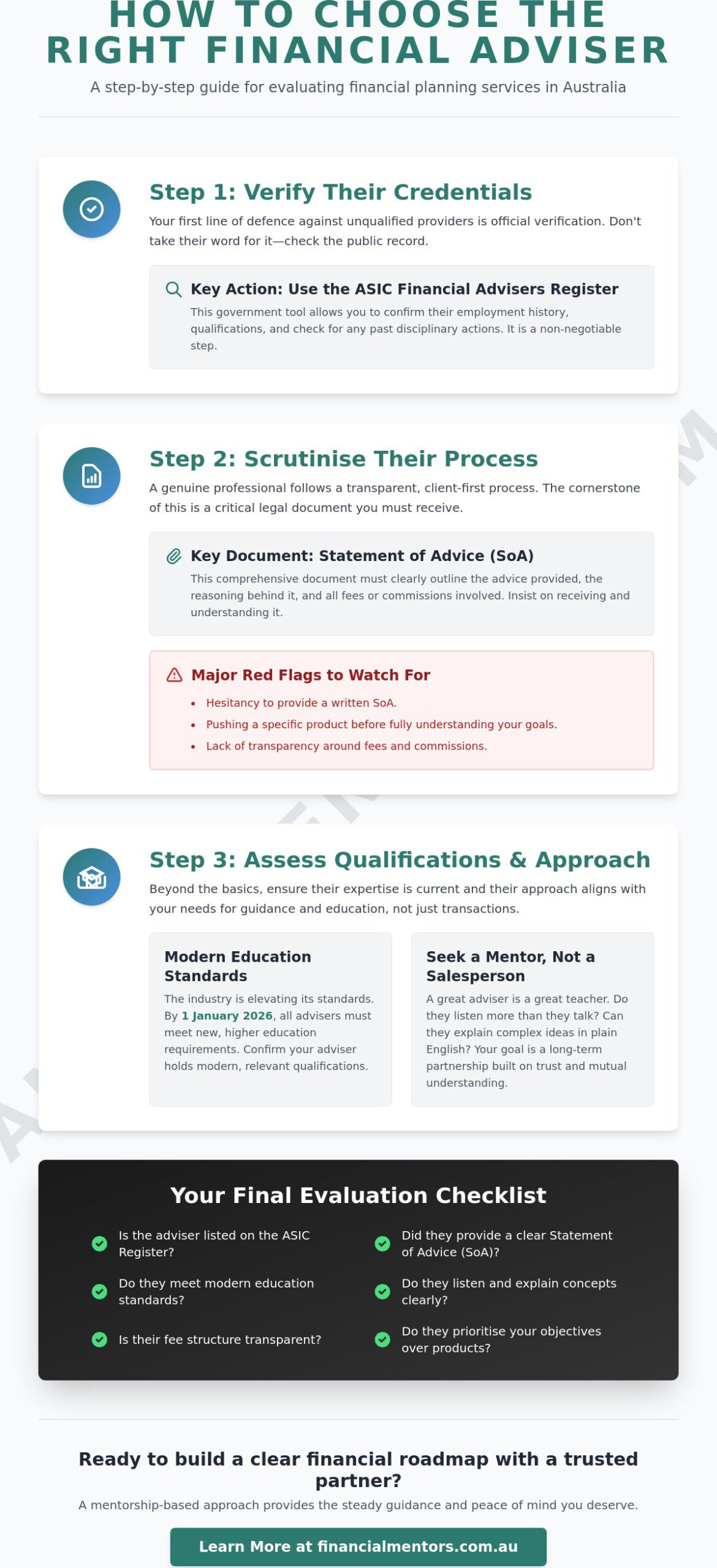

Choosing someone to guide your financial life is a decision based on trust, but it should also be backed by due diligence. With so many options available, how do you distinguish a genuine partner from a mere salesperson? A vital first step is verifying their credentials. In Australia, every professional providing personal advice must be listed on the ASIC Financial Advisers Register. This tool allows you to see their employment history, qualifications, and any disciplinary actions. When choosing a financial adviser, this transparency is your first line of defence against unqualified providers.

Once you’ve confirmed their identity, look closely at their recommendations process. You should always receive a Statement of Advice (SoA). This is a comprehensive legal document that outlines the advice provided, the basis for that advice, and any fees or commissions the planner will receive. If a provider is hesitant to provide an SoA or pushes you toward a specific product before understanding your goals, consider it a significant red flag. Genuine financial planning services prioritise your objectives over their own portfolio of products.

Qualifications and Professional Standards

The industry is currently undergoing a significant shift toward higher professional standards. By 1 January 2026, all existing financial advisers must meet new education standards as outlined in the Corporations Act. This ensures that your adviser isn’t just experienced, but also holds modern, relevant qualifications. However, while degrees and certifications are essential, the “mentor” quality is equally important. Does the adviser take the time to explain complex concepts in plain English? A wise guide will listen more than they speak, ensuring they truly understand your family’s aspirations before suggesting a path forward.

Comparing Fee Structures and Value

Understanding how you pay for advice is crucial for a healthy partnership. Most modern firms have moved toward a fee-for-service model, which offers greater clarity than older commission-based structures. You might encounter upfront fees for the initial plan or ongoing service fees for regular reviews. Before committing, it’s worth understanding the full retirement planning advice cost in Australia so you can assess what transparent, value-driven guidance should look like. It’s also helpful to see how other essentials, like professional tax return preparation, are integrated into your broader strategy. The true value of advice isn’t just a percentage return on an investment; it’s the tax liabilities you’ve minimised, the estate complications you’ve avoided, and the confidence you feel when looking at your retirement timeline.

Strategic Retirement and Estate Planning: Securing the Future

What does a truly successful retirement look like to you? For many Australians, it isn’t just about the day they stop work, but about the decades of life that follow. Transitioning from the accumulation phase, where you focus on growing your nest egg, to the decumulation phase, where you begin to live off it, requires a significant mental and strategic shift. This is where financial planning services prove their worth, moving beyond simple investment picks to help you curate a sustainable, dignified income stream that lasts as long as you do.

A resilient retirement plan typically balances three distinct pillars: your superannuation, private savings, and potential Age Pension entitlements. As of March 2026, the maximum Age Pension rates sit at $1,200.90 per fortnight for singles and $1,810.40 for couples. Understanding how your private assets interact with Centrelink’s deeming rates, which are currently 1.25% for lower thresholds and 3.25% for assets above those limits, is essential for maximising your benefits. If you don’t yet meet the asset tests for the pension, your strategy might focus on drawing down private wealth effectively while waiting for eligibility. Knowing how to choose a financial adviser who understands these nuances can make a substantial difference to your long-term cash flow.

Bridging the Retirement Income Gap

If you aren’t quite ready to stop work entirely, a transition-to-retirement (TTR) strategy can be a wise middle ground. This allows you to access a portion of your super while you are still working, helping you reduce your hours without sacrificing your lifestyle. A key focus here is managing longevity risk. With Australians living longer than ever, your roadmap must account for inflation and the rising costs of healthcare. Regular reviews are vital, especially with proposed changes like the new tax arrangements for super balances over $3 million expected to apply from 1 July 2026.

Estate Planning Advice for Modern Families

Your legacy is about more than just a list of assets; it’s about the people you leave behind. Professional estate planning advice ensures that your wealth reaches your loved ones in the most efficient way possible, which is particularly important for blended families or those with complex asset structures. Consider the following essentials to protect your family’s harmony:

- Binding Death Benefit Nominations: Ensuring your super goes directly to your intended beneficiaries, bypassing potential legal challenges.

- Minimising “Death Taxes”: Strategically managing how super benefits are paid to non-dependants to reduce the tax burden on your children.

- Powers of Attorney: Appointing a trusted person to make decisions on your behalf if you are no longer able to do so.

By treating estate planning as a tool for family stewardship rather than just a compliance chore, you can ensure your hard-earned wealth provides stability and support for generations to come.

The Power of Integrated Tax and Wealth Creation

Many people view tax as an annual obligation to be endured, a once-a-year scramble to gather receipts. But what if you saw your tax return as a powerful lever for growth rather than just a compliance chore? When your tax strategy is integrated into your broader financial planning services, it transforms from a look backward into a proactive plan for the future. By identifying opportunities to reduce your taxable income throughout the year, you can significantly increase your investable surplus. This extra capital, when managed wisely, becomes the fuel for your long-term wealth creation.

The real magic happens when your financial planner and tax accountant work in unison. Instead of you acting as a middleman between two different offices, having these experts “in the same room” ensures that every investment decision is made with its tax consequences in mind. For instance, if you fall into the 30% tax bracket, which applies to income between $45,001 and $135,000 for the 2025-2026 financial year, a strategy like salary sacrificing into superannuation can be highly effective. By utilising the $30,000 concessional contributions cap, you’re effectively paying less tax today while building a larger nest egg for tomorrow.

Tax-Effective Wealth Creation

Strategic wealth creation isn’t just about what you earn; it’s about what you keep. If you have a mortgage, using an offset account or exploring debt recycling can help you turn non-deductible debt into tax-effective investment debt. For long-term investors, understanding Capital Gains Tax (CGT) and how to time the sale of assets is crucial for protecting your returns. In retirement, franking credits from Australian shares can provide a welcome boost to your cash flow, often resulting in tax refunds that further support your lifestyle.

Simplifying the Tax Season

We know that the administrative side of money can feel overwhelming. Professional financial planning services that include tax return preparation take that weight off your shoulders. This integrated approach ensures that every possible deduction is captured within the context of your overall wealth management strategy. It’s about maintaining strict compliance with the ATO while remaining focused on growth. When your records are organised and your strategy is clear, tax season becomes a moment of reflection on your progress rather than a source of stress.

The Mentorship Approach: Why Financial Mentors Wealth Management?

Choosing a partner for your financial journey is about more than just finding a firm with the right certifications. It’s about finding a guide who truly hears your story. At Financial Mentors Wealth Management, we believe that the most effective financial planning services are built on a foundation of clarity and mutual respect. Our founder, Murray Frean, has cultivated a “Wise Mentor” approach that prioritises your unique life milestones over generic data points. We aren’t here to simply manage a portfolio; we are here to walk alongside you as you navigate the complexities of building and protecting your legacy.

Working with an established firm provides a level of stability that is vital in today’s fast-moving market. Having held our Australian Financial Services Licence (AFSL) since 2003, we’ve guided clients through multiple economic cycles, legislative shifts, and personal transitions. This history allows us to provide bespoke advice that rejects the “one size fits all” templates common in larger institutions. Your roadmap is designed specifically for your family, your goals, and your vision of a dignified future. It is a living document that grows as you do.

A Partnership Built on Trust

The discovery phase of our relationship is where the real work begins. It starts with empathetic listening. We want to understand what keeps you awake at night and what you hope to achieve for your children. By simplifying complex financial jargon into plain English, we ensure you feel empowered rather than overwhelmed. Our commitment is to the long-term stewardship of your goals, providing a steady hand and a calm perspective as your circumstances evolve over the years.

Your Next Steps to Financial Peace of Mind

If you are ready to move from uncertainty toward a structured plan, the process is simpler than you might think. To make the most of our initial conversation, it’s helpful to begin organising your financial life. You don’t need to have every detail perfect, but having these items ready can help us build a clearer picture:

- Superannuation Statements: Your most recent reports to help us understand your current trajectory.

- Asset Overview: A general list of your savings, properties, and any existing investments.

- Retirement Aspirations: A few thoughts on the lifestyle you wish to maintain when you stop work.

This initial meeting is an opportunity for us to explore your possibilities without pressure. It’s a chance to see if our mentorship approach aligns with your needs. To begin your journey toward a more secure and confident future, organise a consultation with Financial Mentors Wealth Management today.

Taking the Next Step Toward Your Dignified Retirement

Securing your future is a journey that requires both a clear vision and a steady hand. We’ve explored how moving from simple wealth accumulation to a thoughtful “Planned Retirement” can reduce the stress of outliving your savings. By integrating your tax strategy with your broader investment goals, you don’t just manage your money; you steward your legacy. It’s about ensuring that every decision, from superannuation contributions to estate planning, works in harmony to support the life you’ve worked so hard to build.

Finding the right financial planning services is the most important part of this process. You deserve a partner with the experience to navigate Australia’s shifting legislative landscape. With specialised expertise in retirement and estate planning, and a history as an AFSL registered firm since 2003, we are here to provide the integrated tax and wealth management services you need. If you’re ready to move forward with clarity, start your journey with a trusted mentor at Financial Mentors Wealth Management. Your future self will thank you for the peace of mind you choose today.

Frequently Asked Questions

What is the difference between general and personal financial planning services?

Personal financial planning services are customised to your specific goals, debts, and income, while general advice is broader and doesn’t account for your unique situation. If you receive personal advice, your planner has a legal obligation to act in your best interests. This ensures the strategy fits your life perfectly, rather than being a generic suggestion that might not suit your tax bracket or family needs.

How much do financial planning services typically cost in Australia?

Fees for financial planning services in Australia depend on the complexity of your situation and whether you require a one-off plan or ongoing mentorship. Most professional firms now use a fee-for-service model, providing clear transparency regarding what you pay. For a detailed breakdown of what to expect, our guide to retirement planning advice cost in Australia outlines current fee structures and how to assess their value. It’s always best to ask for a clear breakdown of upfront and ongoing costs during your initial conversation to ensure the value aligns with your personal goals.

Do I need a lot of money to start working with a financial planner?

You don’t need to be wealthy to begin. In fact, early planning is often the most effective way to build long-term security. Many people start with wealth creation strategies while they are still in the workforce to maximise their superannuation and manage debt. If you have a clear goal for the future, a mentor can help you find the most efficient path to get there, regardless of your current balance.

What should I look for in a Statement of Advice (SoA)?

A Statement of Advice (SoA) should clearly outline the recommendations made and the specific reasons why they are right for you. It’s a legal document that must also disclose all fees, commissions, and any potential conflicts of interest. When you review your SoA, ensure that the “Scope of Advice” matches what you discussed and that the path forward feels practical and achievable for your circumstances.

Can a financial planner help me with my tax return preparation?

Yes, some firms provide integrated support that includes professional tax return preparation alongside your broader investment strategy. This approach is highly beneficial because it ensures your annual tax obligations are handled with your long-term wealth goals in mind. By having your tax and planning experts working together, you can identify more opportunities to reduce liabilities and increase your investable surplus throughout the year.

How often should I review my financial plan with my advisor?

Most Australians benefit from a formal review at least once a year to ensure their roadmap remains on track. However, you should also reach out if you experience a major life milestone, such as a career change, receiving an inheritance, or starting a family. Regular check-ins allow your strategy to evolve alongside changes in legislation, such as the new superannuation tax arrangements expected from 1 July 2026.

Is estate planning advice included in standard financial planning?

Holistic financial planning typically includes estate planning advice to ensure your hard-earned assets are protected for the next generation. This involves more than just writing a will; it covers binding death benefit nominations for your super and strategies to minimise the tax burden on your beneficiaries. It’s a vital tool for maintaining family harmony and ensuring your legacy is handled exactly as you intended.

What is an AFSL and why is it important for my protection?

An AFSL, or Australian Financial Services Licence, is a mandatory requirement for any business providing financial advice in Australia. It’s a sign that the firm is regulated by ASIC and must meet strict professional and educational standards. For your protection, always verify that your advisor is an authorised representative of an AFSL holder. This ensures you have access to formal dispute resolution schemes if any issues arise.