What if the difference between a comfortable retirement and a stressful one wasn’t how much you saved, but how you structured what you already own? It’s a question many Australians face as they approach 67, often feeling a sense of unease that the age pension asset limits might unexpectedly reduce their fortnightly income. You’ve worked hard to build your nest egg, and it’s only natural to feel anxious about how your personal belongings, investments, and superannuation are valued by Centrelink.

If you’re worried that the taper rate might eat into your lifestyle, then you aren’t alone. We understand that seeing your payment reduced by A$3 for every A$1,000 over the threshold can feel like a penalty for your success. However, with the right retirement planning, these rules become a framework for stability rather than a hurdle. This guide will help you master the complexities of the 2026 asset testing, giving you the confidence that your assets are structured efficiently to maximise your entitlements.

We’ll explore the specific 2026 thresholds for homeowners and non-homeowners, explain how deeming rates affect your outcome, and provide a clear path toward securing both your lifestyle and your legacy.

Key Takeaways

- Learn how Centrelink applies the lower result of the income and assets tests to determine your final fortnightly payment rate.

- Discover why your family home is generally an exempt asset and how age pension asset limits vary significantly for homeowners and non-homeowners.

- Understand the impact of the taper rate and how small changes in your assessable assets can affect your overall retirement budget.

- Explore practical ways to organise your wealth, such as investing in your principal place of residence, to support your lifestyle while remaining compliant.

- Identify how professional retirement planning can help you navigate these complex thresholds with confidence and peace of mind.

Understanding the Age Pension Asset Test in 2026

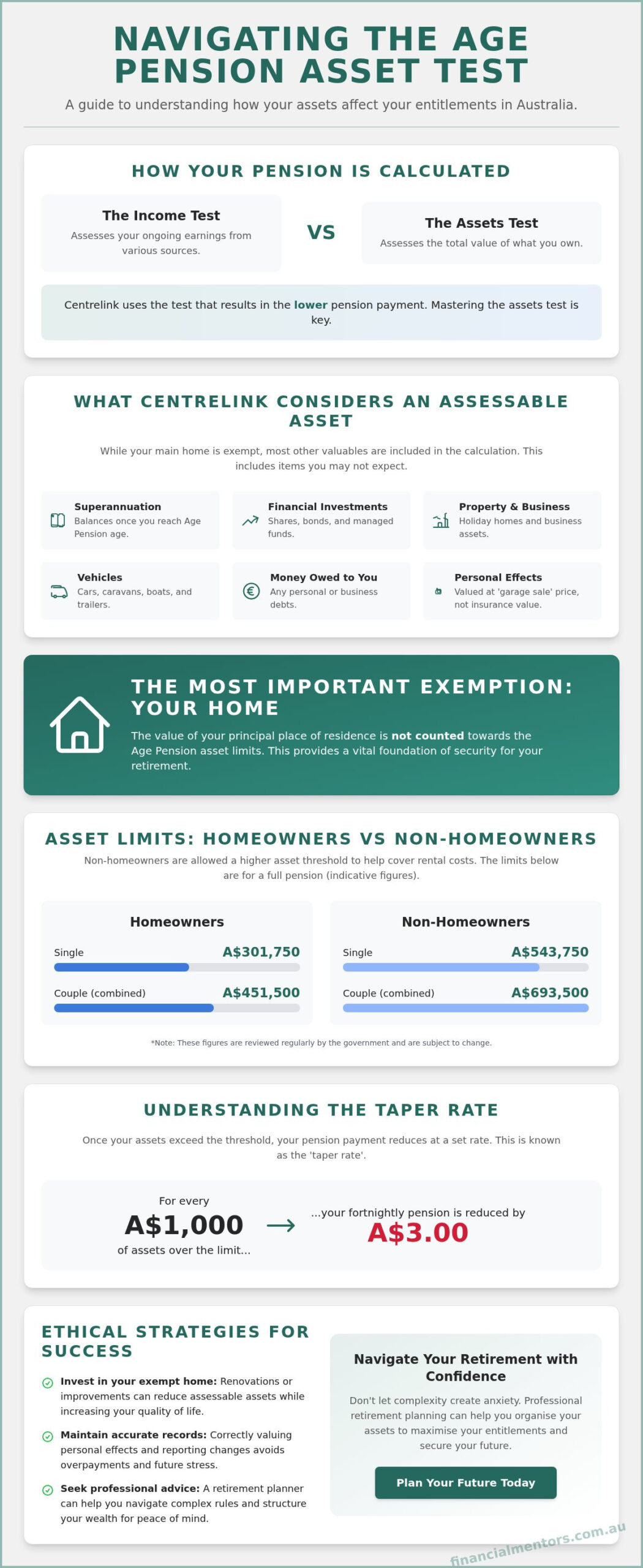

Entering retirement often brings a mix of excitement and quiet apprehension. You’ve spent a lifetime working, saving, and making sacrifices to build a future for yourself and your family. It’s completely natural to feel protective of those savings. Within Australia’s social security system, the Age Pension is designed to provide a safety net, but it’s governed by two main pillars: the income test and the assets test. Centrelink looks at both, and the test that results in the lower payment amount is the one they apply to your fortnightly rate.

If your income is low but your assets are high, the asset test will likely be the one that determines your pension. Conversely, if you have few assets but a higher income, the income test takes the lead. Understanding the age pension asset limits is essential because these figures aren’t static. To keep up with the cost of living, the government reviews these thresholds every March, July, and September. This ensures the system remains fair as economic conditions shift, though it does mean you’ll need to stay informed to keep your retirement plan on track.

What counts as an asset for Centrelink?

Many people are surprised by what Centrelink considers an assessable asset. While bank accounts and investment properties are obvious, your superannuation balance also joins the list once you reach the Age Pension age of 67. It’s the “hidden” items that often catch retirees off guard. Household contents and personal effects are valued at what you could get for them at a garage sale, not their replacement cost. Other assessable items include:

- Caravans, boats, and trailers

- Financial investments and shares

- Business assets and holiday homes

- Debts owed to you by others

- Assets held outside of Australia

While your principal place of residence is generally exempt, almost everything else you own has a part to play in the calculation. Being thorough in your assessment helps ensure you receive every dollar you’re entitled to.

How the asset test affects your lifestyle

Moving from a regular salary to a combination of private savings and government support requires a shift in mindset. It’s a transition toward stewardship, where you become the careful manager of your accumulated capital. Maintaining accurate records isn’t just about compliance; it’s about peace of mind. If your age pension asset limits are managed correctly through clear reporting, you can avoid the stress of overpayments and the resulting debts. This clarity allows you to focus on what truly matters: enjoying the time you’ve earned with the people you love. By viewing your assets through the lens of long-term stability, you can make informed choices about how to use your wealth to support your lifestyle without fear of “missing out” on the support you deserve.

Current Asset Thresholds: Homeowners vs Non-Homeowners

One of the most reassuring aspects of the Australian retirement system is the treatment of your family home. For the vast majority of retirees, the principal place of residence is an exempt asset. This means its value, whether it’s worth A$500,000 or A$2 million, doesn’t count toward the age pension asset limits. This exemption provides a vital foundation of security, ensuring you have a permanent roof over your head without it impacting your eligibility for government support. It’s a policy designed to let you stay in the community you love while still receiving the assistance you’ve earned.

But what if you don’t own your home? The system accounts for this through a concept often called “renting equity.” Non-homeowners are allowed a significantly higher asset threshold to compensate for the fact that they must pay rent from their private savings. It’s a way of balancing the scales, acknowledging that those without property need more liquid capital to maintain a similar standard of living. Understanding how the assets test is applied across these different living situations is the first step in seeing how your specific circumstances influence your entitlements.

Life can also bring unexpected changes that shift these boundaries. If you and your partner are separated due to illness, perhaps because one of you requires residential aged care, Centrelink typically applies different rules. In these sensitive situations, you are often treated as a “couple separated by illness.” This usually results in higher combined thresholds to help cover the increased costs of running two separate households or paying for care. If you’re unsure how your current living arrangements affect your status, seeking professional retirement planning can provide the clarity you need to move forward with confidence.

Full Pension limits for 2026

As of 20 March 2026, the thresholds for receiving the maximum pension payment are clearly defined. For a single homeowner, your assessable assets must stay below A$321,500. If you’re a single non-homeowner, that limit rises to A$579,500. For couples living together in their own home, the combined limit is A$481,500, while non-homeowner couples can hold up to A$739,500 before their payment starts to decrease. Staying under these amounts ensures you receive the full fortnightly payment.

Part Pension cut-off points

Once you exceed the full pension limits, your payment reduces gradually until it reaches zero at the “upper limit.” For single homeowners, this cut-off point is A$722,000, while non-homeowners can have up to A$980,000. Homeowner couples have a combined cut-off of A$1,085,000, and non-homeowner couples reach the limit at A$1,343,000. Even a small part pension is incredibly valuable, as it typically grants you the Pensioner Concession Card, which provides substantial discounts on medicine, healthcare, and utility bills.

Navigating the Taper Rate and Asset Valuation

Understanding how your wealth translates into a fortnightly budget can feel a little like solving a puzzle with moving pieces. The “taper rate” is one of those pieces. It describes how your pension gradually reduces as your wealth grows beyond the full age pension asset limits. For every A$1,000 you hold above the threshold, your fortnightly payment drops by A$3. While this might seem like a small adjustment, it’s helpful to see the annual impact. For example, if your assessable assets increase by A$10,000, your pension will decrease by A$30 every fortnight. Over a full year, that’s A$780 less in government support.

You might wonder if it’s even worth having extra savings if the pension drops so significantly. It’s a common concern, but it’s helpful to remember that having your own capital usually provides more flexibility than the pension alone. If you have A$10,000 in an accessible account, that money belongs to you for emergencies, repairs, or a well-deserved holiday. The pension is a steady stream, but your assets are your safety net. Finding the right balance between the two is where true financial peace of mind begins. It’s not about having less; it’s about making sure what you have is working for you in the most efficient way possible.

Valuing your personal effects and household contents

When you’re listing your belongings for Centrelink, you don’t need to use the “replacement value” found on your insurance policy. Instead, Centrelink looks for the “resale value.” This is essentially what you could realistically expect to get if you sold your furniture, appliances, and clothes at a garage sale or on an online marketplace. For most people, a lifetime of household items might only be worth a few thousand dollars in this context. When it comes to your car or jewellery, try to find a reasonable second-hand market price. Keeping a simple record of how you arrived at these figures is a wise move, as it provides transparency and confidence if you’re ever asked to explain your valuation.

The interaction between assets and income

Your financial assets, like bank accounts and shares, also play a role in the income test through “deeming.” Centrelink assumes these assets earn a set rate of income, regardless of their actual performance. Currently, the first A$64,200 of a single person’s financial assets is deemed to earn 1.25%, while anything over that amount is deemed at 2.75%. Because Centrelink applies the test that results in the lowest payment, your assets and income are always in a delicate dance. Taking a holistic view of your superannuation, deemed income, and the Age Pension allows you to see your total retirement picture clearly, ensuring your strategy remains stable as you move through this significant life transition.

Strategies for Managing Your Assets Ethically

When you start looking at ways to stay within the age pension asset limits, it’s helpful to view the process as organising your future rather than trying to game a system. You’ve worked hard for your savings, and managing them wisely is an act of stewardship. By understanding the rules, you can ensure your wealth supports your lifestyle while still allowing you to access the government assistance you’re entitled to. This isn’t about hiding assets; it’s about making informed choices that align with your long-term goals and personal values.

One of the most effective ways to manage your assessable assets is to look toward your principal place of residence. Since your home is generally exempt from the assets test, moving funds from a taxable bank account into your home can naturally increase your pension eligibility. However, these decisions shouldn’t be made in a vacuum. It’s vital to consider the five-year look-back rule. Centrelink reviews financial history and gifting for the five years prior to your pension application. This is why early planning is so essential. If you’re considering how to best structure your wealth for the long term, our experts in Retirement Planning at Financial Mentors Wealth Management can help you create a sustainable plan that respects both your needs and the regulations.

Renovating the family home: A strategic move?

If your kitchen is looking tired or your bathroom needs accessibility upgrades, retirement might be the perfect time for a renovation. Spending cash, which is an assessable asset, on home improvements effectively transfers that value into an exempt asset. This can lead to a direct increase in your fortnightly pension payment. Beyond the financial benefits, the lifestyle ROI of a more comfortable, safer, or more energy-efficient home is significant. Just be careful not to over-capitalise. Spending A$100,000 on a renovation that only adds A$50,000 to your home’s value might not be the wisest move if your primary goal is preserving capital for your legacy.

The nuances of gifting and deprivation

It’s only natural to want to help your children or grandchildren, perhaps with a house deposit or education costs. However, Centrelink has strict rules to prevent people from depriving themselves of assets just to get a higher pension. You can gift up to A$10,000 in a single financial year, or a total of A$30,000 over a rolling five-year period. If you exceed these limits, the excess amount still counts as your asset for five years from the date of the gift. This means you could end up with a reduced pension and less cash in your pocket. There are often other ways to support your family without impacting your age pension asset limits, and exploring these options early can save a great deal of stress later on.

Why Professional Retirement Planning is Your Best Asset

Managing your finances in retirement involves much more than simply checking boxes on a government form. While understanding the age pension asset limits is a vital first step, the real value lies in how those numbers fit into the broader tapestry of your life. At Financial Mentors Wealth Management, we act as your trusted guide, sitting across the table to help you navigate these transitions with quiet confidence. We don’t just look at what you have today; we look at where you want to be in ten, twenty, or thirty years. This big-picture approach ensures that your decisions today don’t just satisfy a Centrelink test, but actually build the lifestyle you’ve spent decades dreaming about.

If you’re feeling a sense of unease about whether your savings are enough, then a structured plan can offer the validation you deserve. We acknowledge that your aspirations are unique, and your challenges require personalised attention rather than a one-size-fits-all solution. By partnering with a mentor who understands the emotional nuances of retirement, you can move away from the fear of “missing out” and toward a future defined by stability and choice.

Moving beyond the Centrelink calculator

A simple online calculator can tell you what your payment might be this fortnight, but it cannot tell you if your money will last as long as you do. Professional modelling allows us to project your income streams over several decades, accounting for inflation, market shifts, and your changing health needs. We also provide practical support with Tax Return Preparation, ensuring your affairs remain compliant and efficient as you move through different life stages. By acting as a wise mentor, we take the heavy lifting of financial complexity off your shoulders. This leaves you free to focus on your family and your hobbies, knowing the technical details are in capable hands.

Securing your legacy with Financial Mentors Wealth Management

Your retirement plan is also the foundation of your legacy. Through tailored Estate Planning Advice, we help you ensure that the wealth you’ve worked so hard to protect eventually goes exactly where you intended. Whether you’re looking to support a specific cause or provide for the next generation, having a clear plan reduces the future burden on your loved ones. Our national reach means we’re committed to supporting Australians through all of life’s milestones, providing a steady, methodical hand through both the ups and the downs. If you’re ready to see how your wealth can work in harmony with the age pension asset limits, we’re here to start that conversation. Let us help you plan for a secure and joyful retirement.

Stepping Into Your Future With Confidence

We’ve explored how the 2026 thresholds distinguish between homeowners and non-homeowners, and how the taper rate influences your fortnightly budget. By understanding age pension asset limits and the ethical ways to organise your wealth, you can move away from the anxiety of the unknown and toward a structured, predictable retirement. Whether you’re considering a home renovation or planning a gift for your grandchildren, every decision is a step toward greater financial stewardship.

As specialists in retirement and estate planning advice, Financial Mentors Wealth Management has provided national support to Australian retirees for over two decades. We’re proud to be an Authorised Representative of Financial Mentors AFSL Pty Ltd, serving our community with wise guidance since 2003. If you’re ready to ensure your assets are structured for maximum efficiency and long-term stability, our team is here to walk beside you. Book a consultation with a Financial Mentors advisor today to start your journey toward lasting peace of mind.

Your retirement is a milestone worth celebrating. With a thoughtful plan in place, you can focus on the joys of this new chapter while we help you navigate the complexities of the years ahead.

Frequently Asked Questions

Is the family home included in the Age Pension asset test?

No, your principal place of residence is generally an exempt asset and does not count toward the test. This exemption applies regardless of the home’s market value, provided you are living in it. If you move out of your home permanently, such as entering aged care, the exempt status may change after a specific period of time.

How much can a couple have in assets for the full Age Pension in 2026?

As of March 2026, a homeowner couple can have up to A$481,500 in combined assessable assets to receive the full pension. For couples who do not own their home, this limit increases to A$739,500. These thresholds are designed to provide a fair starting point for government support based on your specific living situation.

What is the “taper rate” and how does it reduce my pension?

The taper rate is the calculation Centrelink uses to reduce your pension once you exceed the full payment threshold. For every A$1,000 of assets you hold above the limit, your fortnightly pension payment is reduced by A$3. This gradual reduction continues until your assets reach the upper cut-off point, at which stage the pension payment stops entirely.

Can I give money to my children to stay under the asset limits?

You can gift money to your children, but you must stay within the strict limits of A$10,000 per financial year or A$30,000 over a rolling five-year period. If you exceed these amounts, the excess is still counted as your asset for five years from the date of the gift. This “deprivation” rule prevents people from quickly reducing their age pension asset limits to increase their payments.

Are my superannuation funds counted as assets by Centrelink?

Yes, your superannuation balance is included in the assets test once you reach the Age Pension age of 67. While super is generally exempt during your working life, it becomes an assessable asset the moment you are old enough to claim the pension. This includes funds held in both accumulation accounts and account-based pensions.

What happens to my pension if I sell my home to downsize?

Proceeds from a home sale that you intend to use for a new principal residence are generally exempt from the asset test for up to 24 months. This window allows you enough time to purchase or build your next home without the sale cash affecting your age pension asset limits. However, any interest earned on that cash while it sits in the bank will still be counted under the income test.

Do overseas assets count towards the Australian Age Pension test?

Yes, Centrelink assesses your global wealth, meaning all assets held outside of Australia must be declared. This includes foreign holiday homes, bank accounts, and business interests. These assets are valued in Australian Dollars using the current exchange rate, and failing to disclose them can lead to significant overpayments and debt recovery actions.

How often should I update Centrelink about the value of my assets?

You are required to notify Centrelink within 14 days of any change that might affect your payment rate. While some financial assets like shares are updated automatically through data matching, you must manually report changes to your cash savings, gifts, or the purchase of new items like a car. Keeping your records current ensures you receive the correct entitlement and avoids the stress of future audits.