Imagine sitting on your verandah on a Tuesday morning, coffee in hand, without the pressure of a looming commute. It’s a beautiful vision, but for many Australians, that peace is often clouded by a single, nagging question: how much will I actually have to live on? When you begin the process of determining retirement income, it is easy to get lost in a sea of spreadsheets and complex regulations. You might worry about whether your super will stretch far enough or how the rising cost of healthcare might impact your plans as you approach the Age Pension age of 67.

It is completely natural to feel a sense of uncertainty when you’re moving away from a regular salary. We understand that you want more than just a survival fund; you want the confidence to enjoy your post-work years without constantly checking your bank balance. This guide provides a clear, step-by-step framework to help you calculate exactly how much income you need to fund your unique lifestyle. We’ll explore current benchmarks like the ASFA comfortable standard, which currently sits at approximately $72,148 per year for couples, and look at how the Age Pension and the $2.1 million transfer balance cap fit into your personal roadmap.

Key Takeaways

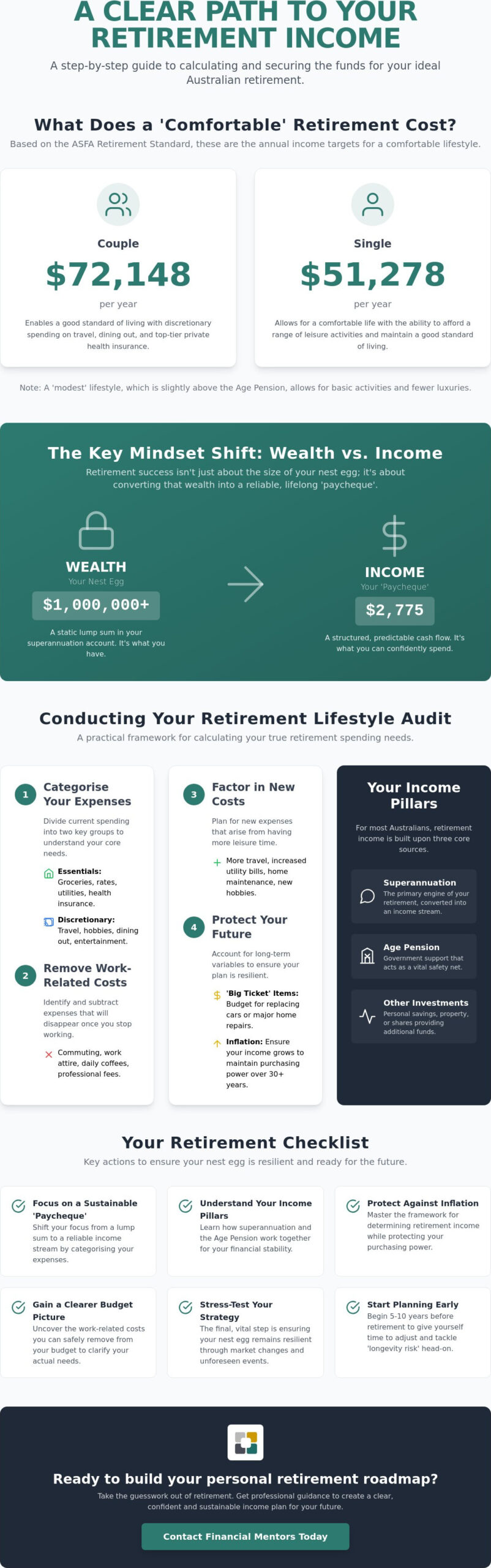

- Shift your focus from a fixed salary to a sustainable “paycheque” by categorising your essential and lifestyle expenses.

- Explore how your superannuation and the Age Pension work together as the primary pillars of your future financial stability.

- Master a practical framework for determining retirement income while protecting your purchasing power against inflation.

- Uncover the work-related costs you can safely remove from your budget to gain a clearer picture of your actual needs.

- Learn why stress-testing your strategy is the final, vital step in ensuring your nest egg remains resilient through market changes.

What Exactly Is Retirement Income and Why Does It Matter Now?

Retirement income is essentially the total cash flow you receive from all sources once you have stepped away from full-time work. It is the engine that powers your new lifestyle. For most Australians, this is a combination of superannuation, government support, and personal savings. The real challenge is not just having the money. It is the psychological shift of moving from a regular salary to “paying yourself” from your own nest egg. We understand that this transition can feel unsettling, but determining retirement income is more than just a calculation; it is about creating certainty for your future self.

Starting the process of determining retirement income early, ideally five to ten years before you finish work, gives you the room to breathe. It allows you to tackle “longevity risk” head-on. This is the technical term for the concern of outliving your capital. Since many of us will enjoy a retirement spanning thirty years or more, your strategy needs to be as resilient as it is flexible. With the average Australian retiree currently living on approximately $2,890 per month, ensuring your capital lasts the distance is a vital part of your long-term stewardship.

The Difference Between Wealth and Income

A $1 million super balance is an impressive achievement, but it is just a number until it’s converted into a usable format. Wealth is what you have; income is what you can spend. We focus on shifting from a lump-sum mindset to a predictable, fortnightly paycheque. This transition ensures your assets are structured to provide consistent support, turning a static pool of funds into a reliable life-line through retirement planning.

Why ‘Rule of Thumb’ Estimates Often Fail

The “70% of your salary” rule is often misleading. It does not account for the unique pressures of the Australian cost of living or your specific health needs. We prefer using the ASFA Retirement Standard as a benchmark. Currently, a couple needs about $72,148 annually for a comfortable life. This provides a realistic foundation for managing Superannuation in Australia based on actual costs rather than arbitrary percentages.

How to Conduct a Retirement Lifestyle Audit

How can you plan for a future if you haven’t yet defined what that future looks like? Determining retirement income starts with a look at your current bank statement, but with a specific twist. We aren’t just looking at what you spend now; we are looking at how those needs will shift when your daily routine no longer revolves around a workplace. If you can visualise your typical Tuesday in ten years’ time, you can begin to put a price tag on it. This audit is the bridge between your current reality and your future peace of mind.

The first step is to categorise your expenses into “Essential” costs, like groceries and rates, and “Discretionary” spending, such as travel or hobbies. You might be surprised to find that many “Work-Related” costs simply vanish. Think about the money you currently spend on commuting, professional attire, and those mid-morning coffees. Once these are removed, you must factor in “New” costs. With more leisure time, you might spend more on petrol for day trips or find your home maintenance needs increase. It’s also vital to adjust for inflation. A lifestyle that costs $60,000 today will likely require a higher figure by 2036 to maintain the same purchasing power. Understanding how your total spend interacts with the Age Pension income test is a crucial part of determining retirement income.

The ASFA Retirement Standard: Modest vs. Comfortable

The Association of Superannuation Funds of Australia (ASFA) provides a helpful reality check for your budget. A “Comfortable” lifestyle in 2026 is defined by the ability to afford overseas travel, dining out, and maintaining a high standard of private health insurance. For a couple, this currently sits at approximately $72,148 per year, while a single person needs about $51,278. A “Modest” lifestyle is slightly above the Age Pension alone but limits you to more basic activities and fewer luxuries. If you’re unsure where your goals sit, a chat about professional retirement planning can help clarify your personal target.

Accounting for the ‘Big Ticket’ Items

Your housing status is perhaps the biggest variable in your audit. Entering retirement with a mortgage-free home provides a level of security that is difficult to overstate. However, you still need to plan for the “lumpy” expenses that occur every decade, such as replacing a car or undertaking major home renovations. We also suggest building a “Health Buffer.” As we age, healthcare costs and private insurance premiums tend to rise, and having a dedicated slice of your income set aside for these needs ensures you aren’t caught off guard by the unexpected.

Mapping Your Income Pillars: Where the Money Comes From

Think of your retirement income not as a single source, but as a collection of streams that flow together to fill your bucket. When you are determining retirement income, it helps to look beyond just your super balance. A resilient plan relies on several pillars working in harmony to provide you with stability and growth. By understanding how these different sources interact, you can create a “paycheque” that is both tax-effective and sustainable for the decades ahead.

For most Australians, these pillars include:

- Superannuation: Your primary engine, often converted into an account-based pension.

- The Age Pension: A government safety net for those who meet the age and means test requirements.

- Private Investments: This might include rental income from an investment property, share dividends, or interest from cash accounts.

- Part-time Work: Many retirees choose to stay engaged through casual work, often utilising the “Work Bonus” scheme to earn up to a certain amount without reducing their pension payments.

Success lies in how you coordinate these elements. If you structure your assets thoughtfully, you can often bridge the gap between a “modest” and “comfortable” lifestyle while maintaining a sense of control over your financial destiny.

Maximising Your Superannuation Drawdown

The move from an “accumulation” account to a “pension” account is a significant milestone. In the retirement phase, your investment earnings are generally tax-free up to the $2.1 million transfer balance cap. You’ll need to meet minimum drawdown rates set by the government, which vary based on your age. This ensures you are actually using your savings for their intended purpose. We often help clients decide whether a “Transition to Retirement” (TTR) strategy is appropriate if they wish to scale back work hours while still contributing to their super.

The Age Pension: A Safety Net or a Foundation?

The Age Pension age is now 67 for all Australians. Currently, the maximum rate for a single person is $1,200.90 per fortnight, while couples receive a combined $1,810.40. Whether you receive a full, part, or no pension depends on Centrelink’s income and assets tests. Determining retirement income involves understanding how your other assets affect these tests. There are legitimate ways to organise your affairs, such as making improvements to your primary residence or gifting within certain limits, that may improve your eligibility. Seeking professional retirement planning advice is often the best way to ensure you are receiving your full entitlements while staying within the rules.

The Variables That Can Derail Your Income Plan

Planning for the future involves more than just looking at the sunny days. Even the most carefully constructed strategy for determining retirement income must account for variables that sit outside your control. Inflation is perhaps the most persistent of these, acting as a silent thief that gradually erodes your purchasing power over a thirty-year retirement. What costs $100 today might cost significantly more in a decade, meaning your “paycheque” needs to grow just to keep pace with the price of milk and bread.

Beyond the cost of living, unexpected life events can also shift your financial foundations. You might find yourself providing financial support to adult children or facing sudden healthcare needs that weren’t in the original budget. Aged care costs are another factor that often appears later in the journey, requiring a level of liquidity that many retirees haven’t fully prepared for. Balancing these risks requires a proactive approach to stewardship rather than a “set and forget” mindset.

Sequence of Returns Risk: The Danger Zone

The timing of market fluctuations matters far more once you begin drawing down on your capital. During your working years, a market dip is often just a chance to buy more units in your super fund. However, if the market crashes in the first few years of your retirement while you are also withdrawing funds, your balance can deplete at an alarming rate. A 10% drop in year one of retirement is harder to recover from than in year twenty. To manage this, we often suggest “bucketing” your assets, which involves keeping several years of cash in a liquid account so you don’t have to sell shares when prices are low.

Tax Planning in Retirement

While most superannuation withdrawals are tax-free for those over age 60, tax planning remains a vital part of determining retirement income. You may still be eligible for the Seniors and Pensioners Tax Offset (SAPTO), which can significantly reduce the tax you pay on income held outside of super. Franking credits from Australian shares can also provide a valuable boost to your spendable cash, often resulting in a tax refund even if your overall tax bill is zero. Because these rules are complex, continuing with professional tax return preparation ensures you aren’t leaving money on the table that could be funding your lifestyle.

From Calculation to Reality: Your Retirement Roadmap

Working through your own budget and exploring the different pillars of support is an excellent first step. However, a “DIY” calculation is often just the beginning of the journey. While a spreadsheet can tell you what might happen in a perfect world, it rarely accounts for the messy, unpredictable nature of real life. When you move from the theory of determining retirement income to the reality of living on it, you need a plan that is as resilient as it is detailed. This is where the transition from a simple estimate to a robust roadmap occurs.

A professional approach involves stress-testing your numbers against thousands of different market scenarios. What happens if inflation stays higher for longer? What if the share market experiences another significant downturn just as you retire? By simulating these possibilities, we can help ensure your strategy doesn’t just work on paper but stands up to the pressures of the real world. This process provides a level of certainty that a basic online calculator simply cannot match, allowing you to move forward with quiet confidence.

It is also vital to remember that your retirement is not a static event. A plan that serves you well at age 65 will likely need to evolve by the time you reach 75 or 85. Your health, your family’s needs, and even your personal goals will shift over time. Ongoing reviews are the key to staying on track, ensuring that your income stream remains aligned with your lifestyle as your priorities change through different stages of your post-work life.

The Value of a Financial Mentor

If you have ever felt the weight of complex financial decisions, you know that professional advice is about more than just numbers. It is about the peace of mind that comes from knowing you have a partner in your corner. We focus on moving the conversation from “can I afford this?” to “how do I best enjoy this?” This shift in perspective allows you to focus on your aspirations while we handle the technical details of retirement planning. We also integrate estate planning advice into your roadmap, ensuring that the legacy you’ve worked so hard to build is protected for the next generation.

Taking Action Today

The best time to start this conversation is now, regardless of where you are in your career or the current size of your super balance. Taking small, deliberate steps today can lead to a far more comfortable tomorrow. To help you get started, consider this final checklist:

- Conduct a thorough audit of your current essential and discretionary expenses.

- Check your latest superannuation statement and familiarise yourself with your current investment options.

- Identify any “big ticket” items, like home renovations or travel, you wish to prioritise.

- Seek professional guidance to stress-test your assumptions.

Your future self will thank you for the stewardship you show today. If you are ready to turn your calculations into a concrete plan, we invite you to start your journey with a complimentary retirement check-in. Let’s work together to create the lifestyle you’ve always envisioned.

Your Journey Toward a Confident Retirement Starts Today

Taking the time to visualise your future is an act of stewardship that pays dividends in peace of mind. By auditing your lifestyle needs and understanding how your superannuation, private investments, and the Age Pension interact, you have already begun the vital work of determining retirement income. It’s about moving past the uncertainty of “what if” and toward the clarity of a structured roadmap that accounts for inflation and market shifts. When you have a clear plan, the focus shifts from managing numbers to enjoying the moments that matter most.

If you’re ready to turn these calculations into a resilient strategy, our authorised representatives are here to walk beside you. With decades of experience, we provide specialised retirement and estate planning advice alongside personalised wealth creation strategies tailored to your unique goals. We invite you to Book a Retirement Planning Consultation with Financial Mentors Wealth Management to stress-test your assumptions and secure your legacy. You’ve spent a lifetime building your nest egg; now it’s time to enjoy the freedom you’ve earned with complete confidence.

Frequently Asked Questions

How much income is enough for a comfortable retirement in Australia?

According to 2026 ASFA standards, a couple generally needs about $72,148 per year for a comfortable lifestyle, while a single person needs approximately $51,278. These figures assume you own your home outright and are in relatively good health. If you plan on frequent overseas travel or have higher medical needs, you may find your personal target sits higher than these benchmarks. It is always best to tailor these figures to your specific aspirations.

Can I get the Age Pension if I have a large superannuation balance?

Your eligibility for the Age Pension is determined by the Services Australia assets and income tests, meaning a large super balance could reduce your payments. While a balance above the thresholds might disqualify you from a full pension, many Australians still qualify for a part-pension once they reach age 67. It is a complex area where careful structuring can help you stay within the rules while maximising your total cash flow.

What is the 4% rule, and does it still work in Australia?

The 4% rule is a traditional guideline suggesting you can withdraw 4% of your initial retirement savings annually, adjusted for inflation, without running out of money. While it provides a helpful starting point, it doesn’t always account for the specific tax environment or market volatility we face in Australia. We often find that a more flexible approach is needed to protect your capital against the sequence of returns risk mentioned earlier in this guide.

Is retirement income from superannuation taxable after age 60?

For most Australians over the age of 60, income drawn from an account-based pension is completely tax-free. This is one of the most significant benefits of our superannuation system, as it allows your savings to work harder for you. However, if you still have funds in an accumulation account or earn income from sources outside of super, you may still need to manage your tax obligations through regular tax return preparation to ensure you are staying compliant.

How do I calculate my retirement income if I still have a mortgage?

If you still have a mortgage, you must treat your monthly repayments as a non-negotiable essential expense when determining retirement income. This significantly increases the total annual figure you need to draw from your assets compared to a debt-free retiree. Some people choose to use a portion of their super as a lump sum to clear the debt, while others prefer to keep the capital invested and pay the mortgage from their ongoing income stream.

What happens to my retirement income plan if the share market crashes?

A market crash can be challenging if it happens early in your retirement, but a well-structured plan should already have protections in place. By keeping two or three years of essential spending in cash or liquid assets, you can avoid selling shares while prices are low. This “bucketing” strategy gives the market time to recover without forcing you to reduce your standard of living or deplete your capital prematurely during a downturn.

How often should I review my retirement income strategy?

We recommend reviewing your retirement income strategy at least once a year to ensure it still aligns with your goals and the current economic climate. Life doesn’t stand still, and changes in government legislation, inflation, or your own health can all impact your original plan. A regular check-in allows you to make small, proactive adjustments rather than waiting for a major problem to arise, keeping you in control of your future lifestyle.

Do I need a financial advisor to determine my retirement income?

While you can certainly start the process yourself, a professional is invaluable for stress-testing your numbers against a wide range of future scenarios. Determining retirement income involves juggling tax laws, Centrelink rules, and investment risks that are often difficult to manage alone. An advisor acts as a wise mentor, helping you move from a place of uncertainty to a position of quiet confidence about your long-term financial security.